Generated by AI

From Days to Minutes: How Indian Banks Can Digitize Merchant Onboarding

5 min

●

ByPriyasy Bokadia

●

18 May 2026

Copy Link

The Onboarding Problem Costing Indian Banks Their Merchant Base

Indian banks aren't losing merchants to payment aggregators because of pricing. They're losing them because of speed. UPI now processes over 700 million transactions per day, 65 million merchants[1] , and accounts for roughly 90% of all retail digital payment volumes in India[1] - yet the merchant base banks can actually onboard into their acquiring systems is growing far slower than the ecosystem itself.

A merchant who walks into a fintech onboarding flow gets a QR code and a live payment account in minutes. The same merchant engaging with a traditional bank's acquiring process encounters document checklists, field agent appointments, and manual KYC reviews - and if they're lucky, a live terminal in one to two weeks. That gap is not a pricing problem. It's a structural one.

Why Merchant Onboarding Still Takes Weeks at Most Indian Banks

Sequential approvals, siloed systems, and field dependencies

The inefficiency is rarely one big problem. It is a chain of small ones, each adding to days. Documents are collected physically - often through a field agent - and manually rekeyed into a Core Banking System. Compliance reviews, risk sign-offs, and operations approvals run sequentially. Each step waits on the previous. A mid-tier bank with reasonable processes can find itself weeks into an application before a merchant ID is generated. EY India's research has highlighted that many Indian banks still require multiple manual touchpoints across merchant activation, even where partial digitization exists. The problem is not the absence of digital tools - it is that those tools have not been connected into an end-to-end automated flow.[2]

Data silos force merchants to repeat themselves

A merchant who already holds a current account with the bank still has to resubmit identity documents for the acquiring onboarding process. The account-opening system and the merchant management system do not share a data layer. Merchants and staff repeat the same verification steps across departments that do not communicate with one another.

Tier 2 and Tier 3 markets add geographic delays

In markets with low branch density, field agents are required for document pickup. This is particularly acute given that around 75% of new QR code deployments in India are now happening in Tier 2 and Tier 3 cities[1] - precisely the markets where branch density is lowest, and field agent dependency is highest. This introduces delays that no amount of internal process optimisation can resolve. The bottleneck is physical, not procedural.

The cumulative cost of field visits, manual rekeying, dropped applications, and compliance headcount inflates the cost per merchant onboarded. For banks targeting scale across India's SME base, this makes merchant acquisition economically difficult to sustain without structural automation.

India already has 665 million QR codes and 11 million PoS terminals deployed - a merchant acceptance infrastructure that has grown 19% over the last three years[1] . The onboarding infrastructure behind it has not kept pace.

How Same-Day Merchant Onboarding Works: The Technical Architecture

Banks that have solved this are not building bespoke internal tools. They are deploying purpose-built merchant onboarding platforms designed specifically for bank-grade compliance and acquiring workflows - delivered as white-label experiences under the bank's own brand.

The architecture has four non-negotiable components.

1. Unified regulatory API orchestration

Aadhaar eKYC, GST verification, PAN validation, and bank account penny-drop verification are integrated into a single orchestration layer that runs all checks in parallel, not in sequence. What previously required a compliance team to verify across four separate databases over two working days is compressed into seconds.

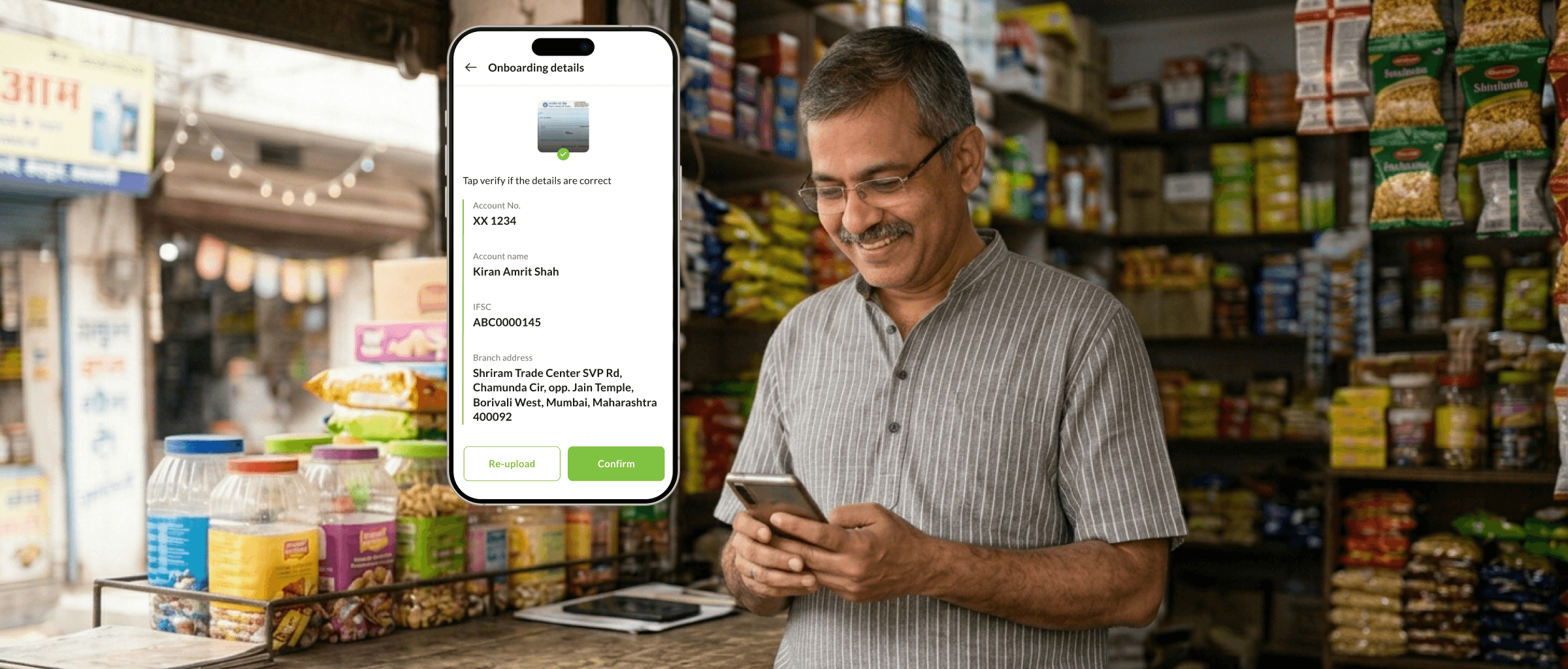

2. Mobile-first, self-serve document capture

Merchants complete the entire journey from their phone. An intelligent capture engine auto-extracts and pre-fills form fields from uploaded documents. This eliminates manual data entry errors, removes the need for branch visits, and makes field agent appointments unnecessary for the majority of applications.

3. Parallel workflow processing

Workflow automation replaces sequential approval chains. Compliance checks, risk scoring, and merchant ID generation are triggered simultaneously upon form submission. The operations team is brought in only for exceptions - not for every application.

4. Deep Core Banking System and payment switch integration

The platform integrates with the bank's Core Banking System and payment switch through clean REST APIs. Merchant ID generation happens without any manual handoff between operations, compliance, and IT teams. What previously required inter-departmental coordination happens automatically, within the same session.

Automated Merchant Risk Assessment: How Compliance and Speed Coexist

Speed without compliance rigour is not a solution - it is a liability. What makes the architecture sustainable is the automated merchant risk assessment layer embedded within the onboarding flow. A configurable risk model evaluates business vintage, transaction history proxies, MCC classification, and negative database matches to generate a risk tier in real time.

The output drives three distinct paths:

-

Low-risk merchants clear immediately through straight-through processing (STP). No human review. Merchant ID generated, QR code issued, account live - within the same session.

-

Medium-risk merchants are routed to a digital review queue with all documentation already collated, enabling faster human review without additional back-and-forth.

-

High-risk applications trigger a structured enhanced due diligence workflow - preserving compliance rigour for the cases that genuinely require it, without applying that overhead to the majority.

Real-time API calls to NSDL, GSTN, and MCA databases validate business identity, tax registration, and director profiles. A process that previously consumed 2 full working days is compressed into seconds. Liveness detection and facial recognition against Aadhaar-linked photographs meets RBI's Video-based Customer Identification Process (V-CIP) standards - eliminating fraudulent identity submissions without requiring video call scheduling or branch-based verification.

What Indian Banks Can Expect After Digitizing Merchant Onboarding

Cycle time compression

Mastercard's research on instant merchant onboarding found that digitized, straight-through processes can compress the merchant activation journey from one to two weeks down to minutes for eligible applications.[3] When the majority of applications qualify for STP - as expected for standard low-risk retail profiles - the onboarding backlog effectively disappears.

Higher activation rates

Lengthy, multi-touchpoint onboarding is one of the primary drivers of abandoned merchant applications. Collapsing the journey into a single mobile session reduces friction at the critical moment when a merchant has decided to sign up. Every percentage point improvement in application completion translates directly into acquiring revenue.

India's SME sector - which contributes 30% to GDP - faces a credit and financial services supply gap estimated at ₹30-35 trillion[1] . Merchant onboarding is the entry point to that relationship.

Structural reduction in cost-to-onboard

Eliminating field visits, physical document handling, manual rekeying, and sequential human approvals removes the largest variable cost items from the process. The cost reduction compounds at scale. It is not linear.

Operations bandwidth reallocation

When operations teams are no longer consumed by data entry and document chasing, that capacity redirects toward relationship management, cross-sell conversations, and portfolio activation. The function evolves from administrative to revenue-generating.

Faster time-to-revenue

Every day a merchant spends in the onboarding queue is a day of transaction volume - and acquiring revenue - lost to the bank, with the online merchant payment market alone projected to reach ₹86 trillion in transaction value by FY30 - growing at a 22% CAGR[1] - the revenue cost of a two-week onboarding delay compounds significantly across a portfolio of thousands of merchants.

Compressing cycle time across thousands of monthly applications has a material impact on the bank's acquiring revenue run rate.

How to Choose the Right Merchant Onboarding Platform in India

Not all platforms are equivalent. For Indian banks, four criteria matter most.

-

Pre-built regulatory connectors. GSTN, MCA21/NSDL, Aadhaar eKYC, PAN, and CIBIL integrations built and maintained by the vendor save months of development time. Building them independently adds cost, time, and ongoing compliance overhead.

-

Acquiring-native features. MCC-based risk configuration, MID generation logic, payment gateway hooks, and settlement account linking must be native to the platform - not bolted on later.

-

Clean API architecture. REST APIs with sandbox environments allow the platform to embed into mobile banking apps, DSA agent portals, and partner channels without full re-platforming.

-

Genuine white label capability. The merchant-facing experience must reflect the bank's brand identity - full branding configuration, communication templates, vernacular language support, and journey-level configuration.

The differentiator between a purpose-built merchant onboarding platform and a generic digital workflow tool is depth. Generic tools handle forms. Acquiring-native platforms handle the full commercial and compliance lifecycle.

Mintoak's DigiOnboard is built on exactly this model - a merchant onboarding SaaS designed for Indian regulatory frameworks, with pre-built connectors to key verification sources. Several of India's leading banks and acquirers, including HDFC Bank, Axis Bank, Yes Bank, and SBI, have deployed have deployed this approach to bring merchants live at scale - collectively empowering over 4.5 million merchants across India and internationally.

The 15-Minute Standard Is Now the Competitive Floor

This is a competitive survival story, not a technology story. Banks that cannot match aggregator onboarding speed will continue to lose merchants - regardless of brand strength, relationship history, or pricing. UPI's continued expansion is accelerating the growth of the merchant payment ecosystem faster than most banks' ability to onboard into it, digital payment volumes in India are projected to grow from 206 billion transactions in FY25 to 617 billion by FY30 - a near tripling in five years[1].The merchant base required to process that volume needs to be onboarded now, not after a two-week approval cycle.

Digitizing merchant onboarding is no longer a transformation initiative reserved for India's largest private banks. It is the baseline expectation for any acquiring institution targeting SME growth. The infrastructure exists today via purpose-built SaaS platforms designed for Indian compliance frameworks - no multi-year build cycle required.

Banks that move in the next 12 to 18 months can recapture merchant segments currently held by fintech aggregators while structurally lowering cost-to-acquire. The compounding effect - faster time-to-revenue, lower cost-per-merchant, higher activation rates - makes this one of the highest-ROI investments available to an acquiring business.

Those who delay risk permanent displacement. Not because aggregators are better banks. Because they got there first.

Frequently Asked Questions

1. Why are Indian banks losing merchants to payment aggregators during onboarding?

It rarely comes down to pricing. The gap is speed. A fintech aggregator can have a merchant live in minutes - QR code provisioned, account active, first transaction ready. A bank running manual KYC collection, sequential compliance approvals, and field agent dependencies can take one to two weeks to reach the same point. By the time the bank's approval clears, the merchant has already transacted elsewhere. Onboarding speed is now a primary competitive variable in merchant acquiring, not a back-office detail, over 84% of industry leaders surveyed believe that low-cost acceptance infrastructure and fast onboarding are critical to driving merchant adoption - and over 90% see the merchant payments segment as having strong growth potential through 2030.[1]

2. What is a digital merchant onboarding solution for banks, and how is it different from generic workflow tools?

A digital merchant onboarding solution built for banks handles the full acquiring lifecycle - KYC and KYB verification, merchant risk assessment, MID and TID generation, payment gateway integration, and settlement account linking - natively, without bolted-on workarounds. Generic workflow tools digitize the form. A purpose-built platform automates the workflow behind it. The difference shows up in straight-through processing rates, compliance auditability, and how quickly a merchant actually goes live.

3. How does automated merchant risk assessment work in bank onboarding?

A configurable risk model evaluates each application across business vintage, MCC classification, geographic risk, and negative database matches - generating a risk tier in real time. Low-risk merchants clear instantly through straight-through processing. Medium-risk applications route to a digital review queue with documentation already collated. High-risk cases trigger structured enhanced due diligence. The result is that compliance rigour is applied where it's needed, without slowing down the majority of applications that don't warrant it.

4. What does white-label merchant onboarding actually mean for a bank?

It means the merchant's entire onboarding experience - the merchant payments app, the communications, the journey flow - reflects the bank's brand, not the technology vendor's. The bank owns the relationship, the data, and the merchant's perception of who onboarded them. White label isn't cosmetic. It matters for merchant trust, for brand continuity, and for the bank's ability to cross-sell into that relationship later without the merchant thinking of a third party as their primary platform.

5. What should banks evaluate when choosing a merchant onboarding platform in India?

Start with Indian regulatory depth - pre-built integrations to Aadhaar eKYC, PAN, GSTN, MCA21/NSDL, and CIBIL are non-negotiable. Building these independently adds months and ongoing compliance overhead. Then assess merchant onboarding API integration quality - clean REST APIs with sandbox environments determine how quickly the platform embeds into mobile banking apps, DSA portals, and partner channels. Also evaluate straight-through processing rates from live Indian bank deployments, configurability of risk rules without code changes, and genuine white-label capability. Licence cost is the smallest part of the total cost of ownership.

6. How much can banks realistically reduce merchant acquisition costs by digitizing onboarding?

The cost reduction comes from removing the largest variable cost items: field visits for document collection, manual data rekeying into core systems, sequential human approvals, and the operations headcount supporting all of it. The savings compound at scale - each merchant onboarded through a straight-through digital process costs a fraction of one processed manually. Beyond direct cost, faster onboarding also means faster time-to-revenue per merchant, which improves the economics of merchant acquisition across the entire portfolio.

India's digital payments ecosystem is on track to process ₹907 trillion in annual transaction value by FY30[1]. For acquiring banks, the cost structure of onboarding determines how much of that revenue they can profitably capture.

_Mintoak's DigiOnboard module is built for exactly this outcome, as a cloud-native, API-first merchant SaaS platform operating across 17 countries, Mintoak enables acquirers to deploy, scale, and monetize their SME base - from onboarding through payments, cross-sell, and loyalty - with clients including HDFC Bank, SBI, Axis Bank, Yes Bank, Karnataka Bank, Absa Bank, and Burgan Bank.

_

Learn more at: mintoak.com/products/mintoak-digionboard

References

[1] PwC, 2025 PwC & Global Fintech Fest. (October 2025). The Indian Payments Handbook 2025–2030. Available at: https://www.pwc.in

[2] EY India, 2025 - EY India. (December 2025). Digital Customer Onboarding: The Next Leap in BFSI Customer Onboarding. Ernst & Young LLP, India. Available at: https://www.ey.com/en_in/insights/financial-services/digital-customer-on-boarding-the-next-leap-in-bfsi-customer-on-boarding

[3] Mastercard, 2024 - Mastercard Services. (April 2024). Digital Merchant Onboarding. Mastercard Advisors. Available at: https://www.mastercard.com/global/en/news-and-trends/Insights/2024/digital-merchant-onboarding.html

Share on your socials

Copy Link

Checkout other blogs