Generated by AI

How African Banks Can Digitise KYC/KYB for Faster Merchant Onboarding

6 mins

●

ByMintoak

●

20 May 2026

Copy Link

Summary

- Manual KYC/KYB onboarding in Nigeria, South Africa, and Kenya takes days or weeks - fintech competitors are doing it in minutes.

- Each market has distinct regulatory requirements: CAC and BVN in Nigeria, FICA and CIPC in South Africa, eCitizen and KRA PIN in Kenya.

- A production-grade digital merchant onboarding platform must support both Existing-to-Bank and New-to-Bank merchant journeys with a mobile-first design.

- The ROI case is built on three vectors: lower cost-per-merchant, faster acquisition velocity, and reduced onboarding drop-off.

- Digital KYC/KYB is not a back-office upgrade - it is the entry point to the entire SME banking relationship.

Why Merchant Onboarding Is Broken Across African Markets

Across Sub-Saharan Africa, banks and merchant acquirers are sitting on an enormous opportunity. Millions of informal and semi-formal SMEs are transacting entirely in cash, with no digital payment infrastructure. Yet bringing them into the formal acquiring ecosystem remains painfully slow - primarily because onboarding processes are manual, paper-heavy, and built for a pre-digital era.

In South Africa, Nigeria, and Kenya - three of the continent's most active merchant acquiring markets - the onboarding journey for a new SME merchant still routinely takes days or even weeks. Field agents collect paper KYC documents. Compliance teams manually verify business registration and AML lists. Banks issue terminal IDs only after multiple approval layers.

The strategic stakes are high. Fintechs and mobile money operators across Africa are onboarding merchants in minutes using digital-first KYC/KYB flows. Banks that fail to match this speed risk losing the merchant relationship and all the transaction data and cross-sell revenue that comes with it, to faster-moving competitors.

The African KYC/KYB Challenge: Country-Specific Barriers Banks Must Solve

Compliance requirements across Nigeria, South Africa, and Kenya are not interchangeable. Each market has its own regulatory architecture - and the manual execution of those requirements is where onboarding breaks down.

Nigeria: CAC, BVN, and NFIU Screening

The Central Bank of Nigeria's merchant acquiring guidelines require thorough KYB checks including CAC (Corporate Affairs Commission) registration verification, BVN (Bank Verification Number) validation for merchant principals, and AML screening against NFIU watchlists. Manual execution of these checks across Nigeria's fragmented business registration database creates significant onboarding latency and inconsistency.

South Africa: FICA, CIPC, and Dual Business Structures

FICA (Financial Intelligence Centre Act) compliance mandates customer due diligence for all merchant accounts, including CIPC (Companies and Intellectual Property Commission) verification for business entities and SARS tax clearance checks. South African banks face the added complexity of verifying merchants across both formal (Pty Ltd) and informal (sole trader) business structures, each with different document requirements.

Kenya: CBK Regulations and Mobile Money Complexity

Central Bank of Kenya merchant acquiring regulations require KYB documentation, including verification of the Business Registration Certificate via the eCitizen portal, KRA PIN validation, and beneficial ownership disclosure for entities with transaction values above the threshold. The proliferation of mobile money agent merchants adds further complexity to KYC tiering requirements.

Across all three markets, the common thread is this: compliance is non-negotiable, but the manual execution of compliance checks is what makes onboarding slow, expensive driving merchant drop-off before the acquiring relationship even begins.

A deeper structural challenge underlies this: many African markets have inherited compliance frameworks designed for formalised, first-world economies - frameworks that assume documented business identities, reliable registry databases, and standardised address systems. Applied to highly fragmented, informal economies, these structures create friction that disproportionately excludes the very merchants banks are trying to acquire.

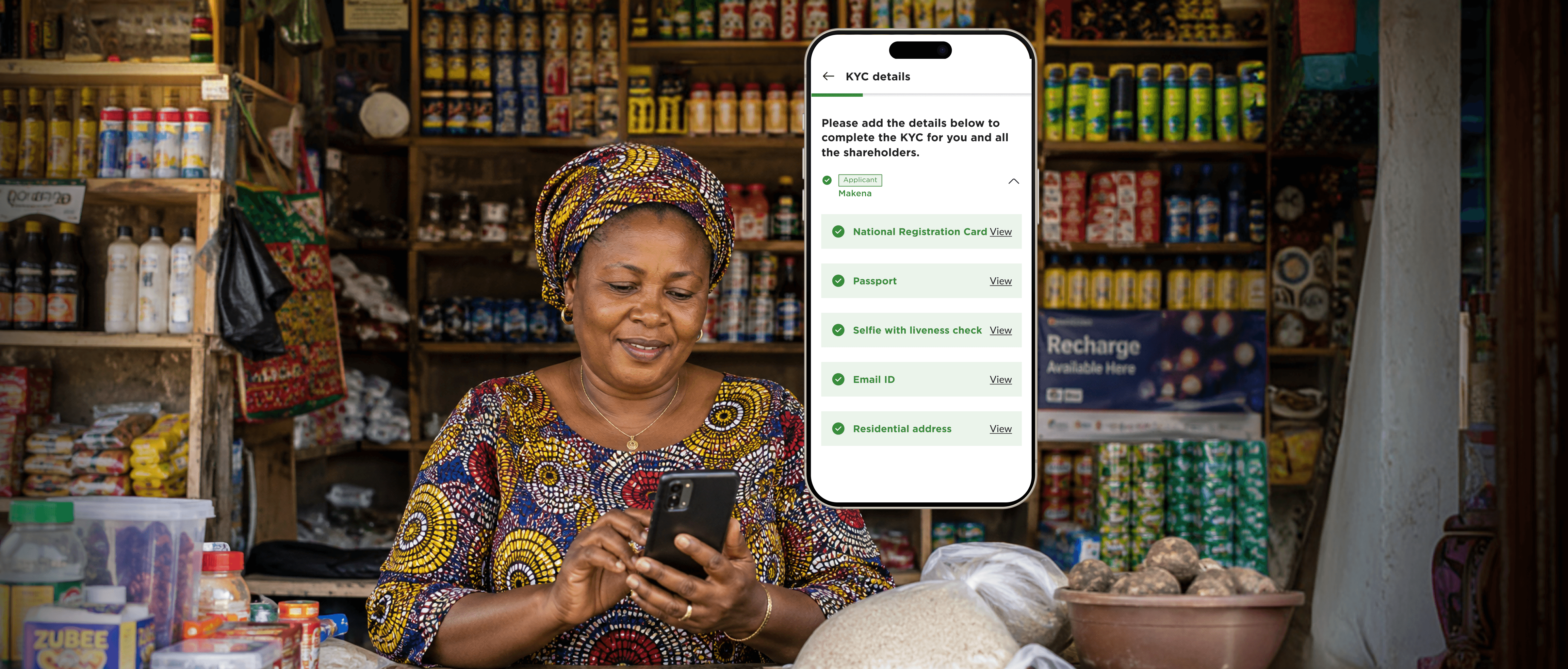

What a Digital Merchant Onboarding Platform Must Deliver for African Banks

A digital merchant onboarding solution for African banks must be built around four core capabilities:

- Seamless API integration with country-specific KYC/KYB data sources

- Real-time AML and sanctions screening against local and international watchlists

- Automated risk scoring that replaces manual compliance assessment

- Instant Merchant ID and Terminal ID generation upon successful verification.

ETB and NTB Merchant Journey Separation

The onboarding flow must support both Existing-to-Bank (ETB) merchants - who can be fast-tracked using the bank's existing KYC data and New-to-Bank (NTB) merchants, who require a full digital KYB journey from document upload through to risk assessment and approval. Treating both groups identically wastes the bank's most valuable asset: its own verified customer data.

Mobile-First Design for Last-Mile Field Agents

Mobile-first design is non-negotiable for the African context. Field agents in Nigeria and Kenya operate primarily on smartphones, not laptops. A digital merchant onboarding platform that requires desktop access or complex document scanning equipment will fail to achieve adoption at the last mile and will push agents back to paper-based workarounds.

White-Label Configurability

African banks need to maintain their brand identity and embed their own risk policies throughout the merchant onboarding journey. The platform must be adaptable to each institution's workflow approval structures without requiring a full custom development engagement. White-labelling is not optional, it is a baseline requirement for regulated institutions protecting their brand relationship with merchants.

What to Look for When Evaluating a Digital Merchant Onboarding Platform

Country-Specific Regulatory Fit

Country-specific regulatory fit should be the first filter. A platform that works for one African market will not automatically work for another. KYC/KYB data source integrations, AML screening requirements, and document verification rules differ meaningfully between Nigeria, South Africa, and Kenya. Evaluate whether the platform can be configured per market without a full re-implementation.

Field Agent Usability

Field agent usability is as important as backend compliance capability. The most sophisticated KYB engine will deliver poor results if field agents revert to paper because the mobile interface is cumbersome. Evaluate platforms on the agent experience - document capture, form completion, and submission confirmation - not just on what happens in the back office after submission.

Data Residency and Governance Controls

Data governance and residency controls are non-negotiable for regulated institutions. South African banks operating under POPIA and Nigerian banks subject to NDPR need clear contractual and technical guarantees on where merchant data is stored and processed. This should be a procurement requirement, not an afterthought during implementation.

The Business Case: Quantifying the ROI of Digital KYC/KYB in Africa

For those evaluating investment in a digital merchant onboarding platform, the ROI case is built on three measurable vectors.

-

Reduction in cost-per-merchant-onboarded - replacing field agent time, manual document processing, and back-office compliance review with automated digital flows.

-

Increase in merchant acquisition velocity - more merchants onboarded per month with the same or smaller operations team.

-

Reduction in onboarding-stage drop-off - faster time-to-first-transaction means less attrition before the acquiring relationship generates revenue.

Banks that have implemented digital onboarding solutions report meaningful improvements in onboarding throughput compared to manual processes, with speed gains concentrated in the KYC verification and risk assessment stages - the two bottlenecks that automation directly eliminates.

Beyond operational savings, the strategic value of digital KYC/KYB lies in the merchant data captured at onboarding: verified business identity, transaction history, and risk profile data that enables the bank to immediately begin cross-selling working capital loans, business insurance, and payment acceptance devices. Onboarding cost becomes the starting point of a long-term merchant banking relationship.

Top management should also model the compliance risk reduction value. Automated audit trails, consistent document verification, and real-time AML screening reduce the exposure to regulatory penalties that manual onboarding processes - with their inherent inconsistency and documentation gaps - routinely create.

Frequently Asked Questions

1. What is digital merchant onboarding and why does it matter for African banks?

Digital merchant onboarding replaces paper-based KYC/KYB collection with automated, API-driven verification flows. For African banks operating across high-growth markets like Nigeria, South Africa, and Kenya, it means onboarding SME merchants in hours instead of weeks. The commercial case goes beyond speed - every merchant onboarded digitally generates verified identity and transaction data that supports cross-selling financial services from day one.

2. What are the KYC/KYB requirements for merchant onboarding in Nigeria?

The Central Bank of Nigeria requires merchant acquirers to conduct CAC registration verification, BVN validation for merchant principals, and AML screening against NFIU watchlists. These checks must be documented and auditable. A digital merchant onboarding platform for Nigeria must integrate directly with these data sources via API to perform checks in real time rather than through manual back-office processes.

3. How does FICA compliance affect merchant onboarding in South Africa?

FICA mandates customer due diligence for all merchant accounts opened by South African banks, including business registration verification through CIPC and SARS tax clearance confirmation. The complexity increases because South African banks must handle both formal company structures and informal sole trader merchants, each with different document requirements. A digital onboarding platform must be configurable to manage both flows within the same compliance framework.

4. What is the difference between ETB and NTB merchant onboarding flows?

ETB (Existing-to-Bank) merchants are businesses that already hold accounts with the acquiring bank. Their KYC data is partially or fully verified, allowing the bank to accelerate onboarding by reusing verified information. NTB (New-to-Bank) merchants require a full digital KYB journey from document submission through to risk scoring and approval. Platforms that treat both groups identically miss the opportunity to dramatically reduce onboarding time and cost for the ETB segment.

It is also important to acknowledge that merchant acquiring onboarding carries obligations beyond standard KYB - Visa and Mastercard scheme rules require acquirers to conduct MATCH (Member Alert to Control High-Risk) checks, internal credit assessments, and in many cases physical site visits before a merchant can be boarded. Digital platforms must be built to accommodate these requirements within the automated flow, not treat them as exceptions.

Platforms must also account for the physical reality of informal merchant locations - where street addresses often do not exist and site visits are costly. Geo-tagging and image capture capabilities on mobile allow merchants to verify their location digitally, reducing dependence on field visits without compromising due diligence.

5. What is the difference between ETB and NTB merchant onboarding flows?

ETB (Existing-to-Bank) merchants can be fast-tracked using the bank's existing verified KYC data. NTB (New-to-Bank) merchants require a full digital KYB journey from document submission through to risk scoring and approval. Beyond this distinction, merchant acquiring carries additional obligations - Visa/Mastercard MATCH checks, credit assessments, and site visits. Platforms must handle these within the automated flow, including geo-tagging and image capture for merchants in informal settlements where street addresses don't exist.

6. How does DigiOnboard support merchant location verification where street addresses don't exist?

Many informal merchants across Africa operate in settlements without recognised street addresses, making traditional address verification unreliable and physical site visits expensive. DigiOnboard solves this through mobile geo-tagging and store image capture, allowing merchants to pin their precise GPS location and upload photos of their business premises directly from their smartphone. This creates a verifiable, auditable location record that satisfies due diligence requirements without the cost and logistics of a field visit - enabling banks to onboard last-mile merchants faster, at lower cost, and at greater scale.

7. How does a digital merchant onboarding platform reduce compliance risk for African banks?

Automated onboarding platforms create consistent, auditable records of every verification step - document capture, AML screening, risk scoring, and approval decisions. This removes the inconsistency and documentation gaps that characterise manual processes and exposes banks to regulatory penalties. For banks operating under POPIA in South Africa or NDPR in Nigeria, automated data handling with clear residency controls also reduces data governance risk.

8. How quickly can a bank go live with a digital merchant onboarding platform?

Implementation timelines vary by market complexity and the degree of integration required with existing core banking infrastructure. Platforms built on API-first, modular architecture - and designed for white-label deployment - can typically reach production within twelve weeks for a focused market pilot. That said, API availability cannot be assumed across all African markets or all core banking environments. Where direct API integrations are not available, robust deployment requires support for alternative data exchange mechanisms including core banking system integrations and Managed File Transfer (MFT) approaches. Flexibility in integration architecture is as important as the platform's compliance capability. Full multi-country rollout timelines depend on the number of regulatory environments being configured and the bank's internal change management capacity.

9. How quickly can a bank go live with a digital merchant onboarding platform?

Implementation timelines vary by market complexity and core banking integration requirements. API-first, modular platforms designed for white-label deployment can typically reach production within twelve weeks for a focused market pilot. However, API availability cannot be assumed across all African markets - robust deployment must also support core banking system integrations and Managed File Transfer (MFT) approaches. The full multi-country rollout depends on the number of configured regulatory environments and the bank's internal change management capacity.

To see how Mintoak DigiOnboard enables merchant acquirers across Africa to digitise KYC/KYB, onboard merchants instantly, and turn every verified merchant relationship into a platform for deeper financial services delivery, visit mintoak.com/products/mintoak-digionboard.

Conclusion

The window for African banks to establish a differentiated, digital-first merchant acquiring proposition is open - but it is narrowing. Mobile money operators and fintech payment aggregators are already onboarding merchants in minutes across Nigeria, South Africa, and Kenya, and their merchant bases are growing faster than traditional bank-acquired merchant portfolios.

This speed advantage comes with a trade-off: fintechs and mobile money operators typically conduct KYC on the individual merchant owner, bypassing the full KYB verification of the business entity that banks must perform. Banks carry a structurally heavier compliance load - and with it, the ability to build a far deeper, more durable merchant relationship grounded in verified business identity.

Banks that win the African SME acquiring market in the next five years will be those that treat digital merchant onboarding not as a technology upgrade, but as the foundation of their entire merchant banking strategy.

At Mintoak, we recognise that the African SME acquiring opportunity will be won or lost at the onboarding stage - and our Mintoak DigiOnboard platform is built to make sure your bank wins it. Through our active partnerships with banks across Africa, we are committed to replacing slow, manual KYC/KYB processes with digital-first journeys that get merchants transacting faster. This includes support for a tiered onboarding model - where a merchant can receive a provisional MID and begin transacting on a light-KYC basis, with full settlement unlocked only after complete KYC/KYB verification is approved - giving banks a practical path to matching fintech onboarding speed without sacrificing their compliance obligations.

Share on your socials

Copy Link