Generated by AI

Modern Merchant Onboarding for African Banks and Fintechs | Complete Guide

7 mins

●

ByMintoak

●

03 Jun 2026

Copy Link

Summary

- Merchant onboarding is a relationship gateway - not a transactional service. Banks that onboard slowly lose the entire SME banking relationship to faster competitors.

- Fragmented KYC requirements, legacy core systems, and manual approval workflows are the primary operational barriers slowing acquiring growth across Africa.

- A modern digital merchant onboarding platform must deliver mobile-first journeys, real-time KYC/KYB verification, configurable risk tiers, and card scheme compliance natively.

- Regulatory and channel requirements differ significantly by market - Kenya, Nigeria, South Africa, and East African markets each require distinct compliance and UX configurations.

- Four KPIs define onboarding excellence: time-to-active, application completion rate, cost per merchant, and post-activation transaction velocity.

The Merchant Onboarding Imperative Across Africa

Africa's digital payments economy is expanding at a pace that is reshaping the competitive dynamics of merchant acquiring. SMEs and informal traders - long underserved by traditional banking infrastructure - are now the primary merchant segment that banks, MNOs, and fintechs are competing to acquire at scale.

Despite this growth opportunity, many financial institutions across Kenya, Nigeria, Ghana, Uganda, Tanzania, Zambia, Botswana, and South Africa still rely on paper-heavy, branch-dependent onboarding processes that delay merchant activation by days or even weeks. The gap between what merchants now expect - shaped by mobile-first experiences in every other part of their commercial lives - and the operational reality of traditional onboarding has become a significant competitive liability for incumbents.

This guide provides a framework to evaluate, modernise, and scale merchant onboarding capabilities. The focus is practical: what to fix, how to measure it, and what a production-grade digital onboarding platform must deliver across African markets.

Why Merchant Onboarding Is a Strategic Priority, Not an Operational One

Merchant acquiring is no longer just a transactional service. It is a relationship gateway that enables cross-sell of business accounts, lending, insurance, and value-added services to SMEs. The bank that onboards a merchant first sets the terms of that commercial relationship - including which financial products the merchant is introduced to, and when.

Fintechs and super-apps are aggressively undercutting traditional institutions by offering same-day merchant registration. The pressure to reduce merchant onboarding time is no longer a back-office efficiency argument - it is an existential competitive one.

Every day a merchant is not active represents lost interchange revenue, missed data capture, and a window for a competitor to establish the banking relationship first. Institutions that master fast merchant onboarding gain a compounding advantage: faster portfolio growth, richer transaction data, and stronger merchant loyalty over the long term.

The Core Challenges Slowing Merchant Acquiring Onboarding Across Africa

Fragmented KYC Requirements by Market

KYC and KYB requirements across African markets are not standardised. CAC registration checks in Nigeria, CIPC verification in South Africa, Business Registration Bureau checks in Ghana - each requires a distinct compliance workflow. Institutions operating across multiple markets are forced to build and maintain separate processes for each country, creating operational silos and compounding the compliance burden as they expand.

Legacy System Architecture

Many banks still require physical document submission and wet signatures, which disproportionately disadvantages micro and small merchants in informal or peri-urban settings without easy branch access. Legacy core banking and acquiring systems frequently lack the API or webhook capabilities needed to integrate real-time verification services, risk scoring engines, or digital signature tools into a unified onboarding workflow.

Internal Approval Workflow Gaps

Poorly defined internal approval processes - often requiring sign-off from credit, compliance, and operations teams working in separate systems - extend time-to-active and create accountability gaps when applications stall. This structural problem is as common as any technology gap, and a digital merchant onboarding platform that does not address workflow orchestration will not solve the speed problem.

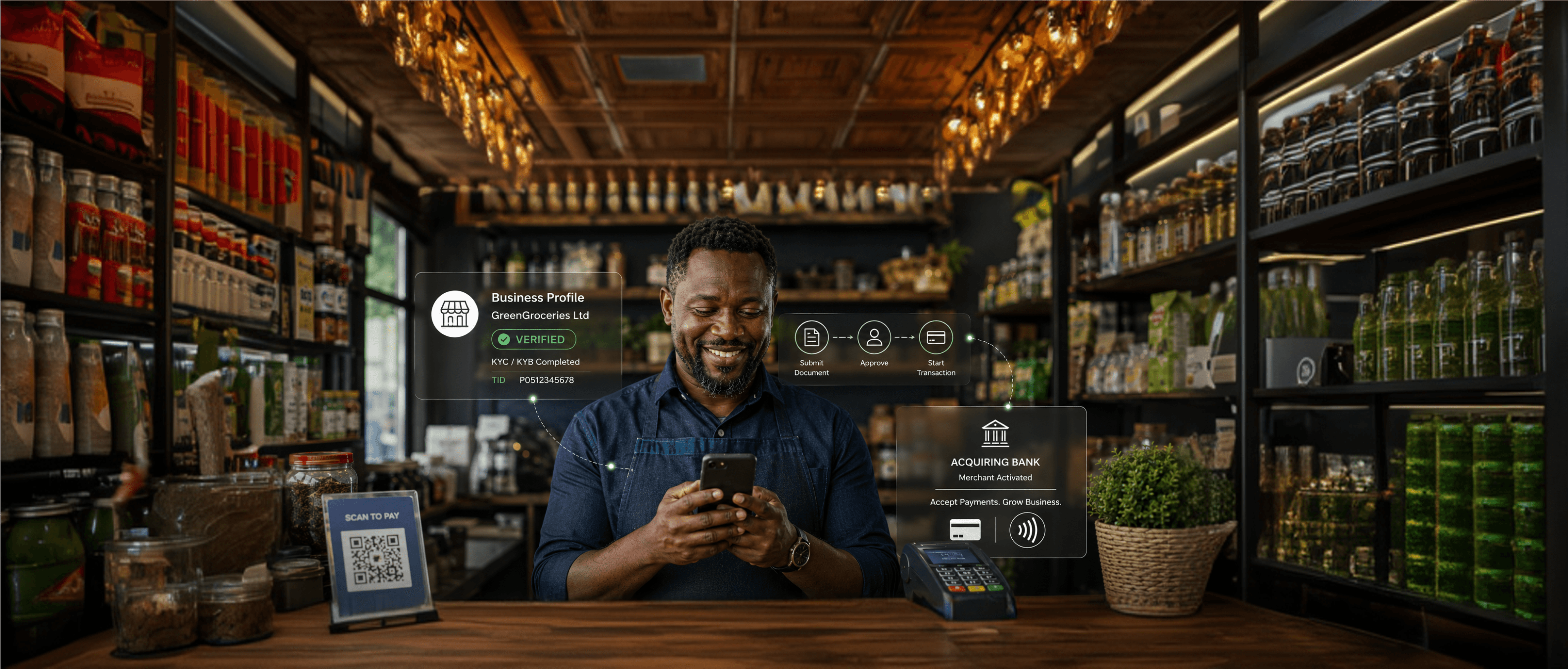

What a Modern Digital Merchant Onboarding Platform Should Deliver

Mobile-First, Self-Service Application Journeys

A best-in-class digital merchant onboarding platform must offer a mobile-first, self-service application journey that allows merchants to submit business details, upload documents, and receive decisions within minutes - not days - directly from a smartphone. In markets where field agents are the primary acquisition channel, the platform must deliver an equally frictionless agent-assisted flow that captures the same data digitally without requiring a branch visit.

Real-Time KYC/KYB Verification

Real-time integration with national ID databases, company registries, and credit bureaus - including providers like TransUnion, Creditinfo, and local market equivalents - is essential to automate KYC and KYB checks without manual intervention. Platforms that rely on batch processing or manual back-office verification cannot achieve the onboarding speeds that the competitive landscape now demands.

Configurable Risk-Based Onboarding Tiers

Platforms should support configurable risk-based onboarding rules so that low-risk micro-merchants are fast-tracked through streamlined tiers while higher-volume merchants trigger enhanced due diligence workflows automatically. This tiering must be adjustable per market without requiring re-implementation - the risk appetite and regulatory baseline differ significantly between markets.

Card Scheme Compliance, Built In

For institutions operating within card scheme ecosystems, compliance with Visa merchant onboarding platform standards and Mastercard MATCH and TMPS requirements must be embedded natively - not bolted on as a post-onboarding step. Platforms that treat scheme compliance as an add-on create delays and audit risk at precisely the point where speed matters most.

Country-Specific Regulatory and Operational Considerations

No single onboarding architecture works across all African markets. The regulatory stack, identity infrastructure, and channel mix differ enough that a market-by-market compliance and UX layer is a prerequisite, not a nice-to-have.

Kenya

Mobile money is the dominant payment rail. Any merchant onboarding platform deployed in Kenya must support mobile money acceptance alongside card acquiring from day one - not as a phase-two addition. Merchant onboarding is regulated under the CBK's National Payment System Act, and platforms must be configured to meet CBK KYB documentation requirements including Business Registration Certificate verification and KRA PIN validation.

Nigeria

The Central Bank of Nigeria's tiered KYC structure - with mandatory BVN and NIN linkage - provides a strong digital identity backbone. Onboarding platforms should automate verification against this infrastructure directly rather than running parallel manual ID checks. The result is faster approvals, cleaner audit trails, and a significantly lower cost per merchant onboarded.

South Africa

Merchant onboarding in South Africa must satisfy FICA identity and AML requirements, POPIA data privacy obligations, PASA payment system rules, and card scheme mandates concurrently. Platforms that address each compliance requirement in isolation create gaps. Multi-regulation compliance must be designed in from the start.

East Africa: Uganda, Tanzania, and Zambia

USSD remains the primary channel for mobile money transactions across much of East Africa. Onboarding platforms serving these markets need USSD fallback capability, offline data capture, and agent-assisted flows to reach merchants outside urban centres. Assuming app-first journeys in these markets will produce adoption failures at the distribution stage.

How to Measure Success: KPIs for Merchant Onboarding Performance

Four KPIs determine whether a digital merchant onboarding programme is delivering commercial results or just replacing one slow process with a digital version of the same problem.

1. Time-to-Active (TTA)

Elapsed time from application start to first merchant transaction. The gap between digital-first acquirers and paper-based processes is measured in hours vs. days. This is the single most visible competitive signal in merchant acquiring.

2. Application Completion Rate (ACR)

Percentage of initiated applications resulting in a fully submitted form. Low ACR signals UX friction, unclear document requirements, or channel mismatch between the platform and the target merchant segment.

3. Cost Per Merchant Onboarded

Digitising onboarding structurally reduces cost-per-acquisition by eliminating field agent visits, manual data entry, and physical document storage. Track this against legacy benchmarks to build and sustain the internal business case.

4. Post-Activation Transaction Velocity

How quickly newly onboarded merchants process their first transaction. A leading indicator of onboarding quality and subsequent retention - monitor across the first week, first month, and first quarter post-activation.

Frequently Asked Questions

1. How can African banks reduce merchant onboarding time without compromising compliance?

The key is replacing manual compliance execution with automated, API-driven verification. Real-time integration with national ID databases, company registries, and AML watchlists allows banks to complete the same compliance checks in minutes rather than days. Configurable risk-based tiers then fast-track low-risk merchants through streamlined flows while routing higher-risk applications to enhanced due diligence - preserving compliance rigour without applying the same delay to every merchant.

2. What are the biggest merchant acquiring onboarding challenges for African banks?

The three most common barriers are fragmented KYC requirements by market, legacy core banking systems that lack real-time API integration capability, and poorly structured internal approval workflows that extend time-to-active independently of any technology constraint. Solving the technology problem without addressing workflow design will not deliver the speed improvements acquiring leaders are targeting.

3. What should a digital merchant onboarding platform for Africa include?

At minimum: mobile-first self-service and agent-assisted application journeys, real-time integration with country-specific KYC and KYB data sources, configurable risk-based onboarding tiers, card scheme compliance built into the workflow, and white-label configurability so the bank maintains brand ownership of the merchant relationship. Platforms that require country-by-country re-implementation to meet local regulatory requirements will not scale across multi-market acquiring programmes.

4. How does fast merchant onboarding affect SME banking revenue?

Speed at onboarding directly determines which institution establishes the primary banking relationship with an SME merchant. The bank that activates a merchant first captures the transaction data, sets the cross-sell sequence, and positions itself for lending, insurance, and value-added services before any competitor enters the picture. Slower onboarding is not just an efficiency problem - it is a revenue leakage problem measured in lost acquiring portfolios and missed cross-sell windows.

5. Is there a Visa merchant onboarding platform standard African banks must comply with?

Yes. Institutions operating within Visa's acquiring ecosystem must adhere to Visa's merchant onboarding standards including merchant registration, risk screening, and ongoing portfolio monitoring requirements. Mastercard's MATCH list and TMPS requirements apply similarly. Both sets of scheme mandates should be embedded natively in the onboarding platform workflow - not handled as a separate post-approval step - to avoid approval delays and scheme compliance exposure.

6. Which African markets present the strongest case for digital merchant onboarding investment?

Nigeria, South Africa, and Kenya represent the three largest and most active merchant acquiring markets on the continent, with established regulatory frameworks and growing digital payment volumes. East African markets including Uganda, Tanzania, and Zambia offer significant merchant acquisition upside but require onboarding platforms with offline capability and USSD fallback to reach merchants outside urban centres. The strongest returns come from platforms that can be configured per market rather than rebuilt for each one.

Conclusion

Modernising merchant onboarding is not a technology project with a defined end date. It is a strategic transformation that requires alignment between product, compliance, technology, and sales teams around a shared objective: frictionless, inclusive merchant acquisition at scale. Institutions that invest in configurable, API-driven digital merchant onboarding platforms will be best positioned to scale acquiring portfolios efficiently across multiple African markets without proportionally scaling operational headcount. The unit economics of digital onboarding improve with volume - manual onboarding does not.

The competitive window is narrowing. Fintechs, telcos, and global card networks are raising the bar for onboarding speed and simplicity. Banks that delay this transformation risk permanent erosion of their merchant acquiring market share to institutions that moved earlier. The next step is an honest audit of the current onboarding process - mapping every handoff, delay, and manual touchpoint - and building a prioritised roadmap toward a fully digital, data-driven merchant lifecycle management capability. That roadmap starts at onboarding, and compounds from there.

Mintoak DigiOnboard gives African banks and fintechs the platform to make that roadmap real automating KYC/KYB, eliminating manual touchpoints, and activating merchants in hours across multiple markets. See how it works at mintoak.com/products/mintoak-digionboard.

To see how Mintoak DigiOnboard enables banks and fintechs across Africa to digitise merchant onboarding, automate KYC/KYB verification, and reduce time-to-active across multiple markets, visit mintoak.com/products/mintoak-digionboard.

Share on your socials

Copy Link

Checkout other blogs