Generated by AI

Merchant Lifecycle Management Automation for Banks and Fintechs in Africa

6 mins

●

ByMintoak

●

26 May 2026

Copy Link

Summary

- African acquirers are signing merchants but losing them within 90 days - lifecycle management automation is the missing layer between onboarding and long-term portfolio value.

- The five stages of merchant lifecycle management - activation, early engagement, growth, retention, and win-back - each require distinct triggers, messages, and incentive mechanics.

- Automated cross-sell logic tied to real transaction milestones outperforms time-based batch campaigns and eliminates the need for field sales visits at every growth opportunity.

- Dormancy prediction models can identify churn risk 30-60 days before a merchant permanently switches, creating a structured intervention window for win-back campaigns.

- A white-label merchant engagement platform with real-time data integration is the operational infrastructure that makes lifecycle automation both scalable and effective.

The Merchant Lifecycle Problem Nobody Is Solving Well

Across Kenya, Nigeria, Ghana, Uganda, Tanzania, Zambia, Botswana, and South Africa, banks, MNOs, and fintechs are acquiring merchants at scale. What most are not doing is keeping them. Merchant inactivity, disengagement, and competitor switching within the first 90 days are eroding acquiring portfolios faster than new merchant sign-ups can replace them.

The root cause is structural. Most acquiring institutions treat merchant management as a one-time onboarding event rather than a continuous lifecycle requiring structured engagement, behavioural triggers, and automated intervention at every stage. Once a merchant is approved and a terminal is issued, the relationship is largely left to chance.

The financial cost compounds quickly. Every dormant merchant represents lost transaction volume, wasted onboarding investment, and a missed opportunity to cross-sell working capital, insurance, or analytics tools.

Closing this gap requires a purpose-built engagement layer sitting between a bank's core transaction infrastructure and its merchant-facing app - one that can translate raw behavioural signals into automated, specific campaigns and targeted segmentation across every channel a merchant actually uses.

Mintoak Engage360 is built specifically around this model - giving acquirers a scalable, structured approach to merchant engagement without requiring a rebuild of their core payments stack. It operates across four layers - dynamic segmentation, multichannel communication (push notifications, SMS, WhatsApp, email), in-app messaging formats like modals, bottom sheets and tooltips, and segmented banners across the merchant app - all configurable by market and merchant segment.

Why Merchant Lifecycle Management Is Broken Across Africa’s Acquiring Ecosystem

Most acquiring teams rely on manual follow-up, fragmented CRM tools, and reactive account management. At small portfolio sizes this is manageable. At scale across Nigeria, Kenya, or Ghana, it is not - and the merchants who drift go unnoticed until they have already switched.

The dominant outreach model - field agents, ignored SMS campaigns, and branch visits - is expensive, does not scale, and is completely disconnected from how modern SMEs actually make decisions. A merchant running a shop in Lagos or Nairobi is not waiting for a relationship manager to visit. They are making financial decisions in real time, inside the apps they already use every day. Institutions that rely on push-based outreach to drive merchant engagement are fighting the wrong battle with the wrong tools. The structural disconnect between onboarding teams, relationship managers, and marketing compounds the problem. Merchants are approved but never activated. Active merchants are never cross-sold. Dormant merchants are never re-engaged. Each failure happens in the gap between teams working in separate systems with no shared view of merchant behaviour.

Market-specific complexity adds another layer. Different regulatory environments, diverse payment rails - Mobile Money, USSD, Card, Tap on Phone, QR - and varying merchant digital literacy mean that lifecycle automation must be configurable by country and merchant segment. A single, undifferentiated outreach sequence applied across all markets will not work.

Without a unified merchant engagement platform, acquirers cannot generate the behavioural data needed to personalise interventions, predict churn risk, or time cross-sell offers correctly. The data exists in transaction systems - but without the automation layer to act on it, it sits unused.

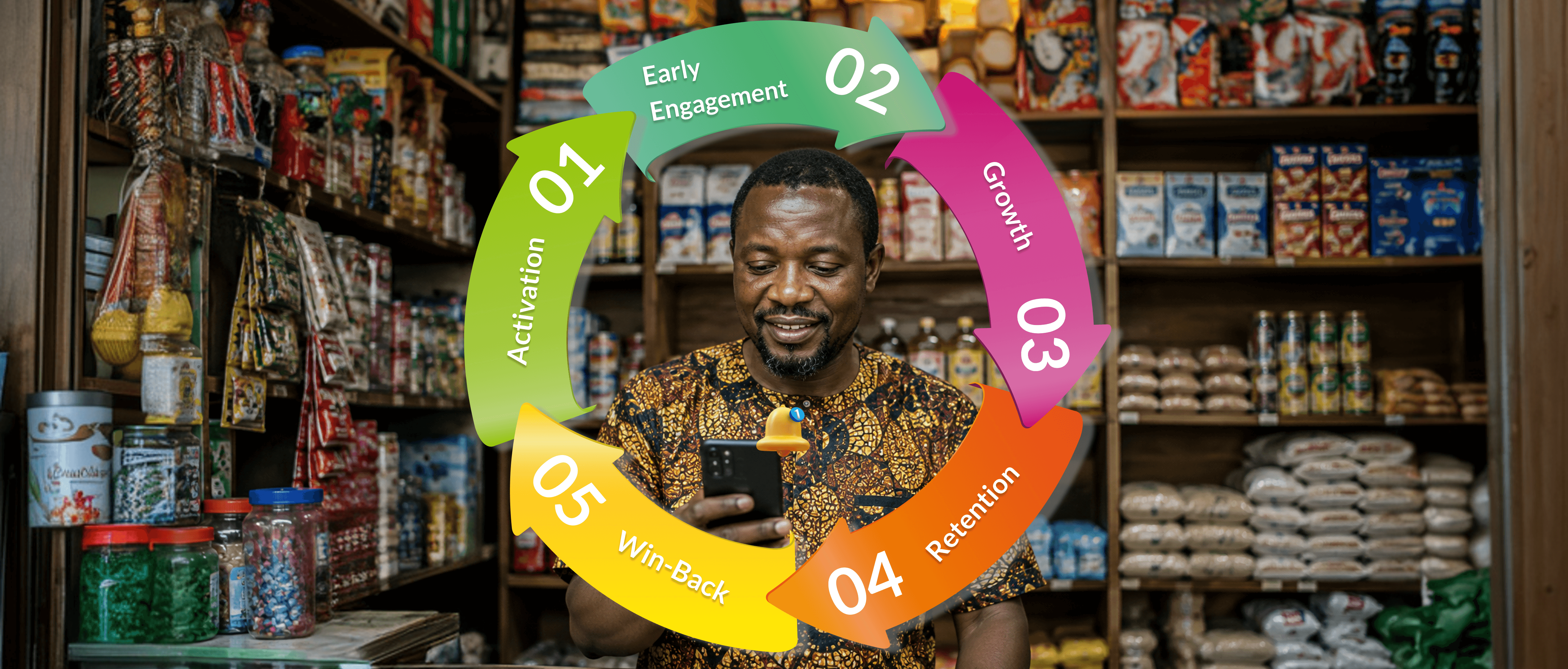

The Five Stages of Merchant Lifecycle Management Automation

A fully automated merchant lifecycle spans five distinct stages, each requiring a different set of triggers, messages, and incentive mechanics. It operates across four engagement layers - dynamic segmentation, multichannel communication (push notifications, SMS, WhatsApp, email), in-app messaging formats like modals, bottom sheets and tooltips, and segmented banners across the merchant app - all configurable by market and merchant segment.

Platforms like Mintoak Engage360 use event-driven logic to move merchants between stages based on real transaction data, app engagement signals, support history, and product usage patterns.

At the activation stage, the goal is to reduce time-to-first-transaction. Guided onboarding flows, proactive SMS or WhatsApp outreach, in-app screen takeovers, and agent-assisted nudges triggered by inactivity signals compress the window between approval and the merchant's first live transaction.

At the early engagement stage, push notifications and in-app tooltips walk merchants through settlement flows and key features - reducing drop-off before habits are formed.

By the growth stage, automated cross-sell logic surfaces the right financial product - an overdraft facility, business insurance, or a loyalty programme - through targeted push notifications, in-app pop-up banners, and email nudges, alongside personalised milestone messages (e.g. "You've completed your 100th transaction - keep going!" or "Your highest transaction value this month was XX"), based on transaction volume thresholds and merchant category codes.

At the retention stage, in-app screen takeovers and personalised push notifications deliver loyalty incentives and business insights directly inside the merchant app at the moment they are most relevant - when the merchant is already engaged with the platform.

For win-back, multi-channel orchestration combining WhatsApp messages, email nudges, and in-app screen takeovers triggered on the merchant's next app open significantly outperforms single-channel approaches - particularly in markets with high mobile penetration and low email engagement.

Retention and Cross-Sell Automation: Growing Merchant Wallet Share

Merchant retention in competitive acquiring markets like Nigeria and South Africa is no longer about transaction fees alone. It requires consistently delivering value through business tools, analytics dashboards, settlement transparency, and personalised growth insights that make switching costly. The data bears this out: 55% of merchants on app-based platforms actively engage with financial products beyond payments, and conversions are 4.5x higher when those offers are embedded inside the merchant app rather than pushed through external channels. This is the shift that separates a payment provider from an SME growth partner - and it is one of the most significant commercial repositioning opportunities available to acquirers today. Platforms like Mintoak Engage360 are built around this insight - giving acquirers the infrastructure to make that shift without rebuilding their core payments stack.

See how smarter merchant engagement can drive app adoption and unlock new revenue opportunities.

Automated cross-sell campaigns triggered by milestone events - a merchant’s first 100 transactions, reaching a monthly GMV threshold, expanding to a second terminal - create commercially relevant moments to introduce value-added services. These triggers are grounded in the merchant’s own behaviour, which makes them land differently from generic promotional messages.

Behavioural segmentation within Engage360 - built on real merchant app behaviour and live transaction data - lets acquirers differentiate between high-potential micro-merchants who need digital literacy support and established SME merchants ready for working capital products. Every cross-sell message reaches the right merchant at the right moment - not because a relationship manager remembered to follow up, but because the platform automated it.

Win-Back Campaigns: Reactivating Dormant Merchants Before They Are Gone

Dormancy prediction models embedded in the Mintoak merchant lifecycle management platforms identify merchants at high churn risk between 30 and 60 days before they permanently switch - creating a critical intervention window that reactive account management consistently misses.

Effective win-back campaigns in African markets must account for the fact that merchant dormancy often reflects operational rather than satisfaction issues: a lost SIM card, a broken terminal, seasonal slowdowns, or cash flow stress. Outreach that addresses root causes directly - with a fee waiver offer, a device replacement trigger, or a working capital prompt - outperforms generic re-engagement messages.

Multi-channel win-back automation significantly outperforms single-channel approaches in African markets - particularly where mobile penetration is high and email engagement is low. Effective campaigns combine WhatsApp messages, email nudges, agent call triggers, and in-app screen takeovers triggered on the merchant's next app open, with outreach that addresses the root cause of dormancy directly - a fee waiver offer, a device replacement trigger, or a working capital prompt - rather than sending a generic re-engagement message. Mintoak Engage360 builds this orchestration layer into the platform natively, so banks and fintechs with structured win-back programmes turn what was previously passive attrition into a manageable, measurable recovery asset.

What to Look for in a Merchant Lifecycle Management Platform

Not all merchant engagement platforms are built for the operational reality of African acquiring. Three capabilities separate platforms that deliver commercial results from those that add complexity without impact.

White-Label Capability

Merchant-facing apps, communications, and dashboards must carry the bank’s or MNO’s brand - not the vendor’s. Merchant confusion about who owns the acquiring relationship erodes trust and, over time, retention. A white-label merchant engagement platform preserves the institution’s brand equity throughout the entire merchant lifecycle.

Real-Time Data Integration

Lifecycle triggers only work if they are based on real-time transactional data, not stale exports. Native integration with core banking systems, POS management platforms, mobile money rails, and CRM is the infrastructure requirement that separates functional lifecycle automation from batch-processed campaign management dressed up as something more sophisticated.

Built-In Cohort Analytics

Activation rates by merchant category, cross-sell conversion by region, win-back success by channel - these are the analytics that let acquiring teams make data-driven decisions across campaigns and success events, refining lifecycle strategy on evidence rather than intuition. Platforms that require data to be exported into a separate BI tool before it can be acted on introduce the same lag that lifecycle automation is designed to eliminate.

Frequently Asked Questions

1. What is merchant lifecycle management and why does it matter for African banks?

Merchant lifecycle management is the structured approach to engaging, retaining, and growing merchants across every stage of the acquiring relationship - from first transaction through to long-term portfolio value. For African banks and fintechs operating in high-churn, high-competition markets like Nigeria, Kenya, and South Africa, it is the operational layer that converts onboarding investment into sustained revenue. Without it, a significant share of newly acquired merchants become dormant within 90 days, and the cost of acquiring them is never recovered.

2. What are the most effective merchant retention strategies for banks in Africa?

The most effective merchant retention strategies combine behavioural triggers with personalised outreach rather than relying on time-based batch campaigns. Automated alerts tied to real transaction milestones - a drop in weekly transaction frequency, a merchant reaching a GMV threshold, or a terminal going offline - allow acquiring teams to intervene at the right moment with the right message. In African markets, multi-channel delivery via WhatsApp, SMS, and in-app push notifications consistently outperforms email-only retention programmes.

3. How does a merchant engagement platform support cross-sell automation?

A merchant engagement platform surfaces cross-sell opportunities by monitoring real-time transaction data against pre-configured thresholds and merchant profiles. When a merchant crosses a defined transaction volume, their category code matches a product eligibility criteria, or they reach a milestone like their 100th transaction, the platform delivers a targeted offer - for a working capital loan, business insurance, or a loyalty programme - without requiring a field sales visit or manual CRM update. This is what separates merchant cross-sell automation from traditional relationship management.

4. What should a white-label merchant engagement platform include?

A white-label merchant engagement platform should deliver the full merchant-facing experience - app, communications, dashboards, and notifications - under the acquiring institution’s brand, not the technology vendor’s. Beyond branding, it must offer real-time integration with core banking and payment rails, behavioural segmentation tools, and built-in cohort analytics. Platforms that require vendor involvement for every campaign change will not scale with the pace of merchant portfolio growth.

5. How do win-back campaigns work for dormant merchants in African markets?

Win-back campaigns in African markets work best when they are triggered by predictive dormancy signals rather than waiting for a merchant to become fully inactive. Modern merchant lifecycle management platforms identify churn risk 30 to 60 days in advance, enabling a structured outreach sequence - WhatsApp message, in-app push notifications, agent call trigger, fee waiver offer, or device replacement prompt - before the merchant permanently switches. Effective win-back messaging addresses the root cause of dormancy rather than sending a generic re-engagement prompt, which is why configurable message logic by merchant segment and market is a platform requirement, not a feature.

6. How does merchant lifecycle automation differ from traditional CRM for acquiring banks?

Traditional CRM systems are built for recording and retrieving customer data - they require a human to initiate outreach, update records, and track follow-ups. Merchant lifecycle engagement platforms are built for event-driven action: they monitor transaction data continuously, identify behavioural signals, and trigger personalised interventions without requiring a relationship manager to initiate each touchpoint. For acquiring portfolios of tens or hundreds of thousands of merchants across African markets, this is the operational difference between a scalable engagement model and one that collapses under its own complexity.

Conclusion

For acquiring, digital payments, and SME banking leaders across African markets, AI-powered lifecycle automation is not a future capability. It is the infrastructure needed to compete in an environment where acquisition costs are rising and switching barriers are falling. Institutions that invest now build compounding advantages: lower churn, higher revenue per merchant, deeper data for credit decisioning, and stronger brand loyalty from merchants who experience consistent, relevant engagement throughout their journey - not just at the point of signing.

The shift from reactive account management to automated lifecycle orchestration requires alignment across product, technology, and commercial teams. But the platforms exist to make this achievable in months, not years. The winning acquirers in Africa’s next phase will not be those who sign the most merchants. They will be those who keep them active, grow them intentionally, and win them back when they drift.

Mintoak Engage360 is a Merchant Lifecycle Management platform that empowers acquirers to increase portfolio activation, drive feature adoption, and enable unassisted cross-sell through AI-powered, campaigns that resonate with the business owner across multiple channels. By keeping merchants engaged across their entire lifecycle - through precision targeting , and in-depth campaign analytics - it helps acquiring institutions enhance app stickiness, boost feature adoption, and increase overall payment throughput. Trusted by banks including HDFC Bank, SBI, Axis Bank, Absa, and NMB across 17 countries, Engage360 gives you the infrastructure to engage effectively with your overall merchant portfolio and achieve key business metrics at scale.

Explore Mintoak Engage360 or book a demo to see it applied to your merchant portfolio.

Share on your socials

Copy Link

Checkout other blogs