Generated by AI

Merchant Lifecycle Management for Acquirers: Building a Merchant Engagement Platform for Banks

8 mins

●

ByMintoak

●

17 Jun 2026

Copy Link

Summary

- Indian bank acquirers are onboarding merchants at scale across UPI QR, POS, and Soundbox rails - but post-onboarding engagement is largely limited to settlement SMSes and dispute emails, creating a vacuum that third-party payment aggregators are actively filling.

- A merchant engagement layer is fundamentally different from a transaction app - it is a revenue and relationship engine that actively intervenes at lifecycle moments with personalised content and offers.

- 55% of app merchants actively engage with financial products beyond payments, and conversions are 4.5x higher when offers are embedded inside the merchant app rather than pushed through external channels. [6]

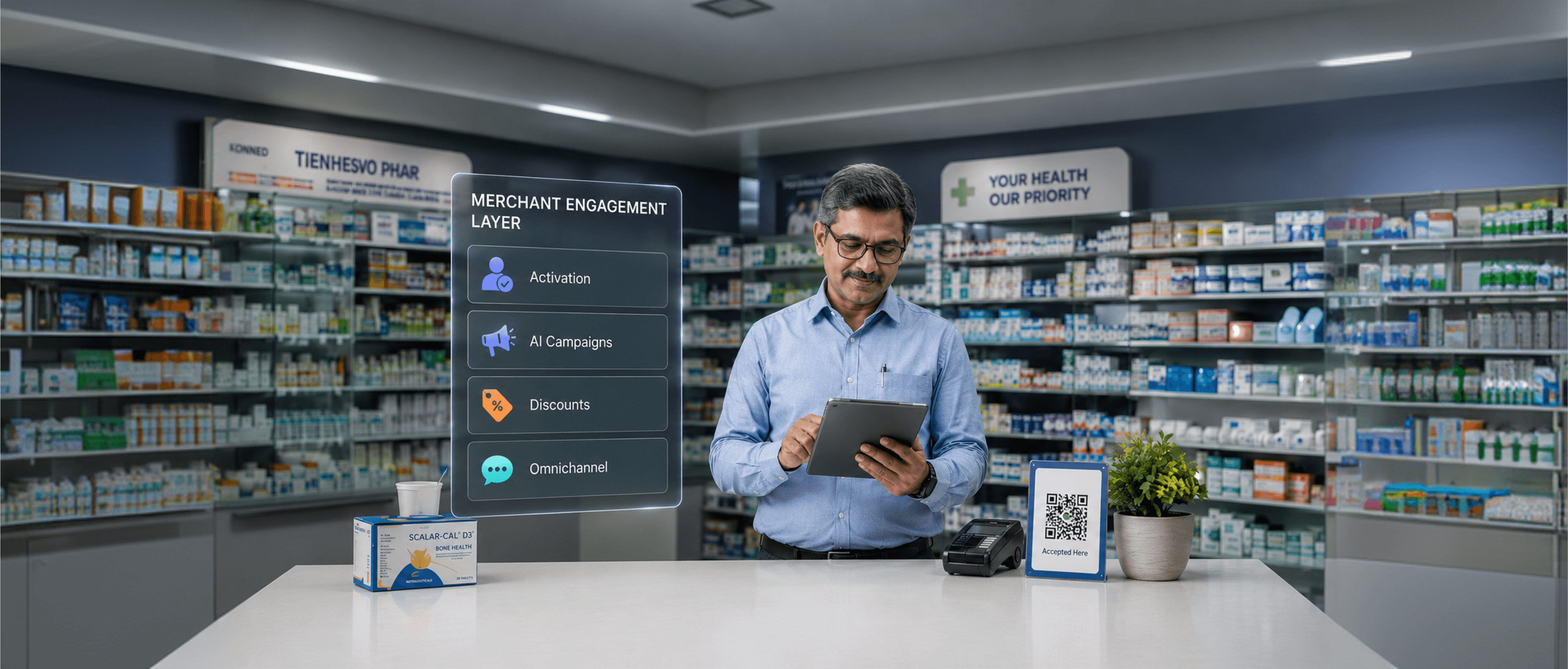

- The five pillars of merchant lifecycle management - activation, behavioural segmentation, AI-driven campaign orchestration, cross-sell automation, and omnichannel communication - are table stakes for any acquiring bank that intends to be a relevant merchant partner in 2026.

- A white-label merchant engagement platform allows acquiring banks to deploy a fully branded engagement infrastructure in weeks, not years, without a multi-year in-house engineering effort.

The Engagement Gap That’s Costing Indian Bank Acquirers Their Merchant Base

There is a quiet crisis playing out across India’s acquiring bank portfolios - and most banks are still treating it as a technology problem. UPI processed 24,162 crore transactions in FY2025-26, with P2M accounting for 63% of total transaction volume. [1] In March 2026 alone, UPI recorded 22.64 billion transactions worth ₹29.53 lakh crore - growing 24% year-on-year in volume. [2] QR codes have expanded to 678 million across the country. [1] The acceptance infrastructure is scaling. The engagement infrastructure is not. For most acquiring banks, the merchant relationship effectively ends the moment the QR code is issued. Post-onboarding interaction is limited to:

- Settlement confirmation SMSes

- Occasional dispute resolution emails

- A field agent visit, once a quarter - if at all

There is no structured lifecycle. No activation programme. No mechanism to flag a merchant who transacted twice after onboarding and then went silent. No trigger tied to the transaction data the bank already holds.

What the engagement gap looks like on the ground

A kirana owner in Nagpur receives a QR code, uses it a handful of times in the first week, and then hears nothing from his bank for three months. No check-in. No transaction insight. No acknowledgement that his business exists beyond the payment rail.

Meanwhile, a fintech aggregator's app sends him a weekly GMV summary, a working capital nudge at week six, and a congratulatory notification when he crosses his 50th transaction. The bank processed every rupee. The aggregator owns the relationship.

This is not a minor operational gap. It is a strategic liability where payment aggregators and fintech-led acquiring platforms have moved decisively to exploit it.

The urgency in 2026 is not abstract. NPCI raised the UPI P2M transaction limit to ₹10 lakh in September 2025, expanding the commercial surface area of every merchant relationship. MSME registrations have crossed 7.94 crore as of May 2026 - up from 6.19 crore at the end of FY 2024-25, adding nearly 1.75 crore new enterprises in a single year. [3] PSU banks are now entering QR-led merchant acquisition territory at scale. [5] The competitive intensity in merchant acquiring has never been higher, and the banks that are building engagement infrastructure now will be significantly harder to displace in 12 months.

Your Merchant Portfolio Is a Financial Asset. Most Banks Are Not Treating It Like One.

The scale of the untapped opportunity is not theoretical. India’s MSME sector has crossed 7.94 crore Udyam registrations as of May 2026. [3] Yet only 18% of Indian MSMEs have accessed digital lending [4] , which means the vast majority of merchants being served by acquiring banks have never received a financial product from the very bank processing their daily payments.

Every acquiring bank processing merchant payments is sitting on a level of transactional intelligence that no credit bureau, no NBFC, and no external fintech can replicate. It knows which merchants are growing, which are seasonal, which are consistent, and which are under stress - before any credit bureau does. That intelligence is generated automatically, with every transaction.

The prize is real. UPI processed 23.2 billion transactions worth ₹29.9 lakh crore in May 2026 - its highest ever monthly volume since launch. [2] P2M accounts for 63% of total UPI transaction volume, with 86% of merchant payments below ₹500, reflecting deep integration into everyday retail commerce - kirana stores, auto fares, roadside vendors. [1] PSU banks have recognised the shift. SBI, Punjab National Bank, and Central Bank of India are now committing resources to QR-code-led merchant acquisition. [5] Raman Khanduja, CEO of Mintoak, articulated why the payment layer is the starting point, not the end point:

“Banks are focusing on making their payment platforms more relevant through features like instant onboarding and on-demand settlement. With an existing strong banking relationship, once the payment layer is solid, adding credit and related products becomes much easier.” [5]

The merchants are already there. The data is already there. The question is whether the bank has the engagement infrastructure to act on it.

A Transaction App Is Not a Merchant Engagement Layer

This is the distinction most acquiring banks are missing and it is costing them.

A transaction app is a passive reporting tool. It shows a merchant their daily settlement. It lets them download a statement and raise a service request. That is useful infrastructure. It is not an engagement tool. It does not intervene. It does not personalise. It does not act.

A merchant engagement layer actively intervenes at key lifecycle moments with relevant, personalised content and offers. It is a revenue and relationship engine built above the transaction stack, integrated with it but not limited to it.

What a transaction app does:

- Reports settlement data

- Handles service requests

- Shows transaction history

What a merchant engagement layer does:

-

Identifies merchants at risk of going dormant - before they do

-

Triggers a personalised reactivation campaign the moment transaction frequency drops

-

Surfaces a pre-approved working capital offer when a merchant’s GMV crosses a threshold

-

Sends a congratulatory message on a merchant’s 100th transaction

-

Delivers a monthly business wrap-up - “Your busiest day was Thursday, your highest transaction was ₹12,000” - that makes the merchant feel seen, not processed

Across Mintoak's client deployments, banks that have built a structured merchant engagement layer have seen 55% of active merchants engage with cross-sell products, and a 4.5x lift in app-driven cross-sell conversions. [6] These numbers come from reaching pre-qualified merchants, in context, through an app they already use every day. The difference is not a feature upgrade. It is a fundamentally different approach to what the merchant app is for.

The Five Pillars of Merchant Lifecycle Management for Indian Acquiring Banks

A merchant engagement layer is built on five interconnected capabilities. Each one addresses a stage of the merchant relationship where most acquiring banks are currently leaving value on the table.

Pillar 1 - Merchant Activation

The first 30 to 60 days post-onboarding are the highest-churn-risk window in the merchant lifecycle. A merchant who does not develop a transaction habit within this window rarely does. Most acquiring banks have no automated mechanism to catch this. The merchant drifts. The QR code gathers dust. And the onboarding investment - the field agent visit, the KYC processing, the terminal deployment - is never recovered.

What activation automation looks like in practice:

- Milestone-based push notifications - first transaction, first settlement, first monthly GMV target - triggered automatically by merchant behaviour, not by a campaign calendar

- In-app screen takeovers for merchants who have not completed their first transaction within 7 days of onboarding

- A congratulatory message on the first successful transaction, the 25th, the 50th, the 100th - small, timed moments that build habit where habit formation is most possible

- WhatsApp nudges for merchants who have gone quiet in the first fortnight.

Catch dormancy before it becomes permanent.

Pillar 2 - Behavioural Segmentation

Dynamic segmentation builds on live behavioural data because not all inactive merchants are inactive for the same reason.

Signal A - Seasonal dip, not churn risk: A textile merchant whose GMV drops in May has likely hit a predictable off-season slowdown. Sending a reactivation campaign here wastes budget and trains the merchant to ignore outreach.

Signal B - Genuine churn risk: A merchant whose transaction frequency has declined for six consecutive weeks, whose app logins have dropped, and who has raised two service tickets - that is a merchant moving toward disengagement. This is the intervention window. Treating both the same way, same message, same channel, same offer - is how engagement campaigns fail.

Dynamic segmentation builds on live behavioural data:

- Transaction frequency trends and GMV trajectory

- App login recurrence and feature usage depth

- Transaction behaviour and dispute patterns

Mintoak Engage360 operates across four configurable engagement layers - dynamic segmentation, multichannel communication (push notifications, SMS, WhatsApp, email), in-app messaging formats (modals, bottom sheets, tooltips, screen takeovers), and segmented banners across merchant app placeholders.

Dynamic segmentation is the infrastructure that makes every other pillar work. Without it, activation campaigns reach the wrong merchants, cross-sell fires at the wrong moment, and omnichannel becomes noise. With it, every subsequent intervention becomes more precise.

Pillar 3 - AI Powered Messaging for Merchant Campaigns

Sending the same communication to 200,000 merchants on the first of every month is not engagement. It is broadcast marketing. Over time, merchants learn to ignore messages that lack relevance to their business.

Mintoak Engage360 helps banks shift from scheduled campaigns to contextual communication. Its AI-powered content assistant enables campaign teams to generate push notification copy in seconds, recommending titles and message bodies under 90 characters (industry standard) based on the campaign objective. Teams can customise language, tone, and intent while retaining full control over the final message.

Combined with an event-driven campaign, this ensures that communication is triggered by merchant behaviour rather than calendar dates. Messages are delivered when they are most relevant:

How it works in practice:

- A merchant’s GMV drops 20% week-on-week - the system triggers an RM alert and a personalised omni-channel communication, not a monthly digest.

- A merchant completes their 50th transaction - a milestone message fires at exactly the moment it lands with meaning.

- A merchant whose highest transaction this month was ₹18,000 receives a message referencing their actual performance - not a generic “Great job!”

- Monthly business wrap-ups - transaction milestones, GMV records, busiest days - are surfaced inside the app, building habitual engagement that makes switching costly.

The objective is simple: make every interaction timely, relevant, and useful. When communication reflects a merchant's actual business activity, engagement improves, and the merchant payments app becomes a merchant engagement app and a valuable part of their daily workflow.

Pillar 4 - The Cross-Sell Opportunity Sitting in Your Transaction Data

India's MSME credit exposure reached ₹46 lakh crore as of April 2026, growing 12.8% year-on-year. [4a] Yet only 18% of Indian MSMEs have accessed digital lending despite 90%+ digital payments adoption. [4] The credit exists. The automated, contextual delivery mechanism - a triggered offer at the right moment, inside the app the merchant already uses - does not, for most acquiring bank portfolios. Acquiring banks already hold the data to close that gap.

A merchant cross-sell platform maps transaction signals to product eligibility:

- A merchant consistently processing ₹5 lakh per month for six consecutive months - likely eligible for a pre-approved working capital loan; the offer surfaces in-app.

- A merchant who has recently added staff logins - a natural prompt for a business current account upgrade

- A merchant approaching a GMV milestone - the right moment to surface a business credit card conversation

- A merchant with six months of clean settlement history - eligible for business insurance cross-sell

The fulfilment design that works: offer surfaces in the merchant payments app, disbursal into the account, repayment auto-debited from future settlements. No collateral. No branch visit. No friction. 44% of app merchants engage with cross-sell products when surfaced contextually within their merchant app. [6] That is not a cold outreach rate. That is what happens when the right offer reaches the right merchant in the right place.

Cross-sell is where the acquiring relationship compounds financially. Every financial product a merchant holds with the bank raises their switching cost, deepens the data signal for the next offer, and increases that merchant's revenue contribution to the acquiring portfolio over time. But none of that matters if the offer never reaches the right merchant, which is precisely what Pillar 5 is built to solve.

Pillar 5 - Omnichannel Communication Orchestration

India's merchant base is not homogeneous. A metro enterprise merchant running five outlets expects seamless in-app analytics and frictionless digital journeys. A Tier-2 and Tier-3 kirana owner who just received their first QR code responds better to a regional-language push notification, WhatsApp message, or SMS - delivered through the channels they actually use daily.

Omnichannel is not about being present on every channel simultaneously. It is about orchestrating a coherent, sequential, context-aware journey across them.

What coordinated omnichannel looks like:

- A WhatsApp nudge for a merchant with declining transaction frequency

- Followed by a reactivation offer via in-app pop-up banner when they next open the app

- Followed by an escalation push notification and in-app banner if there is no response within 72 hours

- All coordinated through one platform - with message fatigue controls, no channel conflicts, and consistent personalisation at every touchpoint

The RBI's Payments Infrastructure Development Fund had deployed approximately 5.45 crore payment acceptance points - QR codes, POS terminals, and soundboxes - across India as of October 2025, many in Tier-3 to Tier-6 cities and the North-East. [1] The merchants now connected through those touchpoints are not reachable through a single-channel approach. Meeting them where they are is not optional - it is how engagement at this scale actually works.

The Revenue Case: What Engagement Unlocks

The zero-MDR reality on UPI P2M transactions means Indian acquiring banks cannot rely on per-transaction fee revenue from the majority of their merchant payment volume. The business case for merchant acquiring depends entirely on the ability to monetise the relationship through value-added services - working capital loans, business insurance, current accounts, fixed deposits, business credit cards.

These are the products that generate margin. They can only be cross-sold to merchants who are actively engaged with the bank’s platform.

India's embedded finance market reached $24.03 billion in 2025 and is projected to reach $27.05 billion in 2026, growing at a CAGR of 8.8% through 2030, with embedded lending and insurance among the fastest-growing verticals. [8] The acquiring bank’s merchant portfolio is the natural distribution channel for that market. But only if the bank has built the engagement infrastructure to surface those products in context.

Raman Khanduja put the broader principle plainly, in the context of data-rich platforms expanding into financial services: “Payments can reveal the minutest details about a customer: when customers spend, where they spend, how often they spend - even a proxy for income profile.” [9]

The acquiring bank already has all of that data on every merchant in its portfolio. The engagement layer is what converts it into timely, personalised action.

Build vs. Buy: Why Most Banks Should Not Build This From Scratch

Building a merchant engagement layer in-house requires integrating:

- A CRM and campaign orchestration engine

- An AI/ML pipeline for segmentation and churn prediction

- Multichannel communication APIs - WhatsApp Business API, push notification infrastructure, SMS gateway

- Real-time merchant transaction and behavioural data connected to the campaign engine in real time

- Lifecycle workflow logic and a merchant health scoring model

This is an 18-to-36-month engineering effort. Most acquiring banks cannot afford that timeline, while fintech competitors fill the gap month by month. A white-label merchant engagement platform purpose-built for bank acquirers can be deployed in a fraction of that time with the bank’s brand, credit policies, and merchant data fully preserved. No ground sales team needed for cross-sell. Targeting, communication, and lead capture happen digitally.

For a detailed look at how this plays out in practice across different markets, read: Merchant Lifecycle Management Automation for Banks and Fintechs in Africa.

The build-versus-buy decision is not binary for every bank. For most mid-size and smaller acquiring banks - where the technology team is already stretched across core banking modernisation and regulatory compliance - building an engagement layer from scratch means ceding 18 to 36 months of competitive ground to aggregators who are already live. The question is not capability. It is timing.

Frequently Asked Questions

1. What is a merchant engagement platform for banks, and how does it drive merchant activation?

A merchant engagement platform for banks manages the full merchant lifecycle from first activation through retention and cross-sell using real-time transaction data, behavioural segmentation, and automated campaigns. For Indian acquiring banks, merchant activation is the most urgent use case: most have no mechanism to catch merchants who go dormant in the first 30 to 60 days post-onboarding. A merchant activation platform deploys milestone-based nudges automatically, converting newly onboarded merchants into regularly transacting ones.

2. What are the most effective merchant retention strategies for banks in India?

The most effective merchant retention strategies for banks in India combine behavioural triggers with personalised outreach rather than time-based batch campaigns. Dormancy prediction flags churn risk 30 to 60 days before it becomes permanent. Milestone-driven engagement - monthly GMV wrap-ups, transaction milestone messages - builds habitual app use. Embedded cross-sell of loans and insurance deepens the financial relationship with merchants. For Tier-2 and Tier-3 merchants, regional-language WhatsApp outreach tends to outperform push-only approaches.

3. How do acquiring banks identify and reactivate dormant merchants before they are lost?

Most acquiring banks have no systematic way to identify dormant merchants until they have already stopped transacting, by which point reactivation is significantly harder and more expensive. A merchant lifecycle management platform monitors behavioural signals continuously: declining transaction frequency, falling app logins, and reduced settlement activity. When these signals converge, the platform can identify churn risk 30 to 60 days before a merchant permanently disengages, creating a structured intervention window. Activation campaigns triggered and delivered through the merchant's preferred channel consistently outperform reactive outreach initiated after dormancy is confirmed.

4. What omnichannel capabilities does a merchant engagement platform need in India?

Effective merchant engagement moves beyond one-size-fits-all communication. Event-driven campaigns enable timely outreach based on merchant actions, business milestones, and transaction trends. An omnichannel platform should coordinate engagement across push notifications, WhatsApp, SMS, in-app messages, and email, supported by audience segmentation, campaign frequency controls, and regional language capabilities. In India, merchant preferences vary widely. While metro merchants often prefer app-based experiences, Tier 2 and Tier 3 merchants engage more actively through WhatsApp, SMS, and regional-language communication. A modern platform must support both through a unified, scalable engagement framework.

5. What should acquiring banks look for in a white-label merchant engagement platform?

A white-label merchant engagement platform must carry the bank's branding across every merchant touchpoint. Beyond branding: real-time integration with core banking infrastructure; built-in campaign analytics for activation rates, cross-sell conversion, and dormancy trends; configurability for RBI compliance; and a proven deployment track record at regulated Indian banks. Speed to market - weeks versus an 18-month in-house build is a significant commercial advantage.

6. How does a merchant lifecycle management solution differ from a traditional CRM for acquirers?

Traditional CRM requires a relationship manager to initiate every outreach manually - unsustainable across lakhs of merchants. A merchant lifecycle management solution for acquirers is event-driven: it monitors transaction data continuously, can identify churn risk 30 to 60 days before disengagement, and triggers personalised interventions automatically. It also delivers portfolio-level cohort analytics across campaigns and lifecycle stages, so acquiring teams can refine their strategy on evidence rather than intuition.

References

[1] PIB/NPCI - April 2026 PIB release: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2257087

[2] The Tribune / ANI (June 2, 2026). UPI Hits new high in May 2026 with 23.2 billion transactions worth Rs 29.9 Trillion, NPCI Data Shows. Available at: https://www.aninews.in/news/business/upi-hits-new-high-in-may-2026-with-232-billion-transactions-worth-rs-299-trillion-npci-data-shows20260602155337/

[3] MSME Ministry, Udyam Registration Portal (May 2026). Udyam Registration data - 7.94 crore registrations. Available at: https://udyamregistration.gov.in/

[4] SIDBI (May 2025). Understanding the Indian MSME Sector: Progress and Challenges - 18% digital lending adoption. Available at: https://www.sidbi.in/uploads/Understanding_Indian_MSME_sector_Progress_and_Challenges_13_05_25_Final.pdf

[4a] CRIF High Mark MSMEx Spotlight Report (June 2026). India's MSME Credit Exposure Reaches ₹46 Lakh Crore Despite Global Uncertainty. Available at: https://www.bizzbuzz.news/national/indias-msme-credit-exposure-reaches-rs-46-lakh-crore-despite-global-uncertainty-1392901

[5] The Economic Times (January 22, 2026). PSU banks counting on QR-based payments to breach a fintech fort. Raman Khanduja, CEO Mintoak, quoted. Available at: https://economictimes.indiatimes.com/tech/technology/psu-banks-counting-on-qr-based-payments-to-breach-a-fintech-fort/articleshow/127036324.cms

[6] Mintoak (2026). Mintoak Engage360 - Merchant Lifecycle Management Platform. Impact data: 44% cross-sell engagement, 55% financial product engagement, 4.5x in-app conversion. Available at: https://www.mintoak.com/products/mintoak-engage360

[7] Reserve Bank of India (May 2025). Reserve Bank of India (Digital Lending) Directions, 2025. RBI/2025-26/36. Available at: https://www.rbi.org.in

[8] ResearchAndMarkets (Q4 2025 Update). India Embedded Finance Market - $24.03 billion in 2025, projected $27.05 billion in 2026, 8.8% CAGR to 2030. Available at: https://www.businesswire.com/news/home/20251124876526/en

[9] The CapTable / Mintoak (August 2025). IRCTC boards the fintech express, eyeing a bigger retail and e-commerce play - Raman Khanduja, CEO Mintoak, quoted. Available at: https://the-captable.com/2025/08/beyond-railway-irctc-payment-licence-fintech-ecommerce-play/

[10] Mintoak (2026). About Us - 4.9M+ merchants, $73B annual GPV, 4.1B annual transactions, 17 countries. Available at: https://www.mintoak.com/about-us

[11] Press Information Bureau, Government of India (April 2026). UPI completes 10 glorious years - 24,162 crore transactions in FY2025-26, ₹314 lakh crore in value, P2M 63% of volume. Available at: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2257087

[12] Outlook Money / Sahamati (May 11, 2026). Account Aggregator ecosystem connects 780 financial institutions, 269 million consents. Available at: https://www.outlookmoney.com/personal-finance/3-ways-account-aggregators-can-save-time-and-simplify-financial-applications-for-loan-or-insurance-seekers

[12a] Business Standard (December 25, 2025). Public-sector banks okay ₹28,724 crore in MSME loans via new digital model — April to October FY26. Available at: https://www.business-standard.com/amp/industry/banking/public-sector-banks-okay-28k-cr-in-msme-loans-via-new-digital-model-125122100503_1.html

[12b] PIB, Government of India (February 2026). Union Budget 2026-27: Building Champion MSMEs for a Global India — ₹10,000 crore SME Growth Fund, TReDS mandate, CGTMSE credit guarantee. Available at: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2228306

Conclusion

The data is already there. The transaction relationship is already there. The competitive window - before aggregators and neo-banks deepen their hold on the relationship is open, but not indefinitely.

UPI processed approximately 24,162 crore transactions worth ₹314 lakh crore in FY2025-26, with P2M accounting for 63% of total transaction volume. [11] India's QR network, the RBI's continued expansion of payment acceptance infrastructure into Tier-3 and beyond, and rising MSME formalisation mean merchant onboarding volumes will continue to grow. Every month without a structured engagement layer is a month in which the bank’s position as an active provider deepens and the cost of reversing that positioning increases.

Merchant acquiring portfolios are not payment infrastructure assets. They are relationship assets - pre-qualified, behaviour-rich, financially underserved cohorts waiting for the bank to show up as a financial partner rather than a settlement machine.

Merchant digital readiness in India has never been higher. What most acquiring banks are still missing is the engagement layer that connects the payment relationship to everything it could unlock.

Mintoak Engage360 is a Merchant Lifecycle Management platform that empowers acquiring banks to increase portfolio activation, drive feature adoption, and enable unassisted cross-sell through AI-powered, contextual campaigns across multiple channels. Trusted by HDFC Bank, SBI, Axis Bank, YES Bank, and Karnataka Bank across India - with 4.9 million+ merchants across 17 countries, $73 billion in annual GPV, and 4.1 billion annual transactions [10] - Engage360 gives you the infrastructure to engage your full merchant portfolio and achieve key business metrics at scale.

Explore Mintoak Engage360 or book a demo to see it applied to your merchant portfolio.

Share on your socials

Copy Link

Checkout other blogs