Generated by AI

The Merchant Retention Blueprint: How Staff Access Makes Your Merchant App Indispensable

6 mins

●

ByMintoak

●

15 Jun 2026

Copy Link

The Silent Attrition Crisis in Bank Merchant Acquiring

There is a churn pattern playing out across Indian acquiring bank portfolios that does not show up in complaint tickets, relationship manager logs, or NPS surveys - because the merchants leaving never complain. They simply move.

The merchants walking out are not the marginal ones. They are QSR chains running 30 outlets in Tier 2 cities, pharmacy franchises processing ₹50 lakh a month, apparel retailers with separate cashier and manager teams across three states. They anchor a bank’s GMV portfolio. And when they migrate to a payment aggregator, the GMV drop arrives before anyone realises the relationship was at risk. The reason they leave is not pricing. It is not the settlement speed. It is not service quality in the traditional sense. It is an operational sophistication gap.

Payment aggregators - BharatPe, PhonePe, Paytm - have invested heavily in merchant-facing features: sub-user creation, outlet-level reporting, cashier access controls, role-based dashboards. Most bank merchant apps remain single-user, single-owner interfaces. The merchant’s operations team has outgrown the platform, and the platform never caught up.

This is not a relationship problem. It is a product decision and it has a product answer.

Why Indian Merchants Are Migrating: The Aggregator Advantage Decoded

The scale of Indian merchant acquiring today is formidable. UPI processed a record 23.2 billion transactions worth ₹29.9 trillion in May 2026 alone - reflecting 24% year-on-year growth in transaction count and 19% in value as of March 2026. P2M payments now constitute a growing proportion of total volumes, reflecting a qualitative shift from peer transfers to a full-fledged merchant ecosystem. [1]

By December 2025, 7,313 lakh UPI QR codes were deployed nationally, far outpacing the 11.2 million physical POS terminals in operation. [2] India’s merchant base has digitised - and it is growing fastest precisely where bank infrastructure is thinnest.

PSU banks have recognised the urgency. SBI, PNB, and Central Bank of India are committing resources to QR-led merchant acquisition, moving into territory long dominated by fintechs. [4] Axis Bank launched “Neo for Merchants,” ICICI built InstaBiz and HDFC Bank scaled Smarthub Vyapar. [5]

But acquiring merchants is one thing. Keeping them engaged is another. And here the aggregator advantage is clearly not in payments infrastructure, but in the merchant experience layer above it. Aggregators have built platforms that serve the merchant’s entire operational team. Banks have historically built for the back office and ignored the front line.

The gaps that drive migration are consistent across mid-market portfolios:

- Bank merchant apps are designed for a single business owner - creating an immediate mismatch with any business that has more than one person managing operations.

- Aggregators offer sub-user creation, cashier access controls, outlet-level reporting, and manager dashboards as standard features most bank apps do not have.

- Multi-outlet merchants crossing five locations represent a disproportionately high churn cohort not due to pricing, but because the bank’s platform stops serving their operational reality. What these merchants need is a multi-outlet staff management app. Merchants running five or more locations cannot be served by a scaled-up single-owner portal. [7]

- By the time GMV drops are visible to the acquiring team, the primary settlement account has typically already migrated.

“Banks are focusing on making their payment platforms more relevant through features like instant onboarding and on-demand settlement. With an existing strong banking relationship, once the payment layer is solid, adding credit and related products becomes much easier.” Raman Khanduja, CEO, Mintoak. [6]

The corollary is equally true: if the payment platform fails the merchant’s operational team, no credit product or relationship manager recovers the account. The product is the relationship.

The Core Gap: Why Single-User Merchant Apps Fail Growing Businesses

Consider what a franchise or retail chain operating 20 outlets actually needs from a franchise payment app: staff access, outlet-level visibility, and role-based delegation built in from the ground up. At minimum, four distinct user types operate simultaneously:

- Cashiers - processing transactions at the counter, needing payment acceptance and nothing else

- Store Managers - reconciling daily settlements, downloading end-of-day reports, managing shift handovers

- Area Managers - monitoring regional GMV across five to ten outlets, identifying underperformers

- Owner / Finance tier - pulling consolidated multi-location reports, managing access rights, controlling the full financial picture.

A single-login portal serves none of them correctly. But this is not just a multi-outlet problem. Even at a single location - a salon, a kirana store, a medical clinic - the owner cannot be present at the counter every hour while also managing suppliers, vendors, and business expansion. The moment a business has more than one staff member touching the payments terminal, the single-user app becomes a structural liability:

- Credential sharing becomes the workaround - one login passed across staff, no audit trail, no access control

- Payment data is visible to all staff, including temporary and part-time employees with no business need for it

- Compliance risk accumulates silently, particularly for merchants with GST filing obligations that require clean transactional records

- The owner remains permanently anchored to daily operational oversight, unable to delegate and focus on growth

The cost of these workarounds - manual Excel reconciliation, informal shift handovers, shared passwords is invisible to the acquiring bank but acutely felt by the merchant’s operations team. It is one of the strongest push factors toward aggregators. And by the time the relationship manager notices the GMV drop, the primary settlement account has already moved.

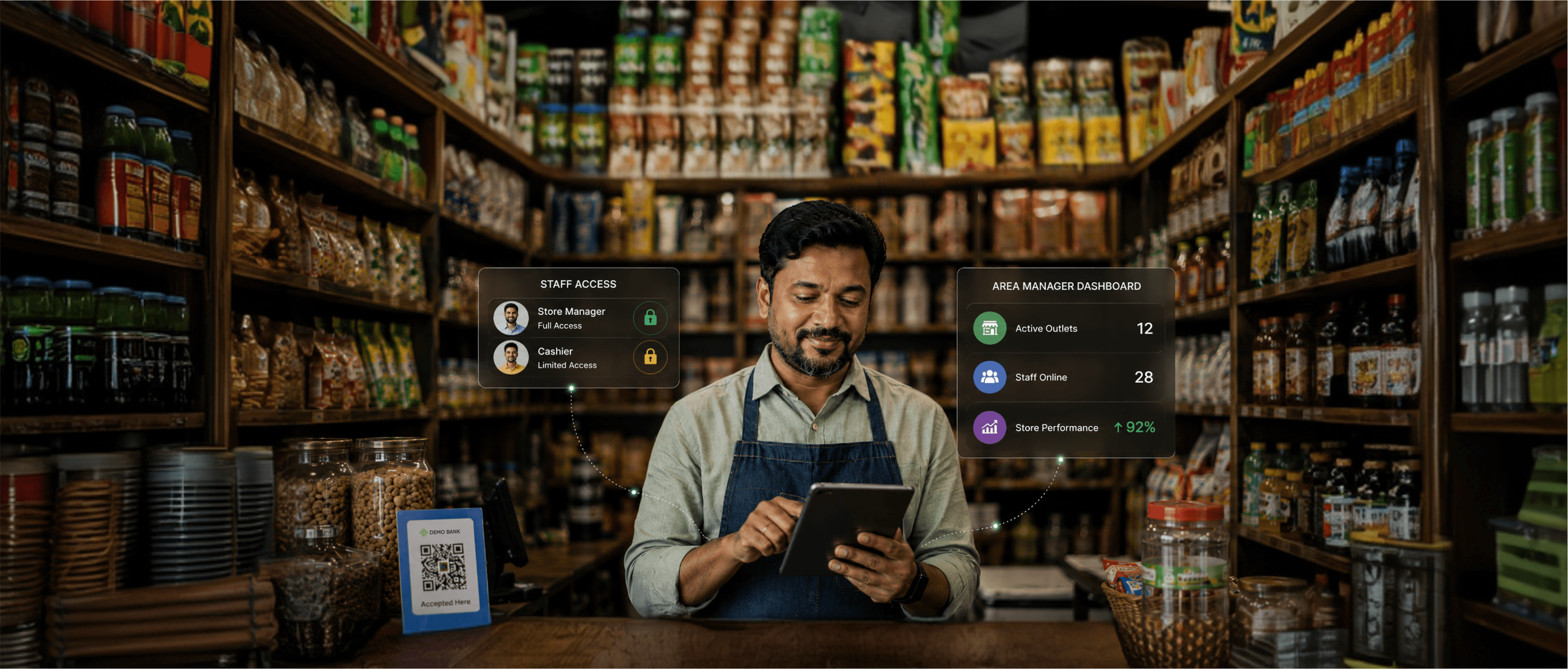

The Staff Access Module: Architecture and Features That Drive Retention

The architecture of a high-retention staff access module is not complicated. But it must be deliberate. For banks operating in India, deploying a staff access module within their merchant payment app is no longer a product differentiator. It is one of the baseline that determines whether the bank retains or loses its growing merchant cohort. Hierarchical role creation is the foundation. A well-designed system supports at minimum four role tiers - cashier, store manager, area manager, and owner - each with configurable permissions over:

- Transaction viewing and payment acceptance

- Settlement data access and report downloads

- Role-based views across multiple business functions

- Access rights delegation to subordinate roles

Mintoak StaffAccess is built precisely around this architecture. A cashier gets payment acceptance only. A store manager gets reconciliation and report access for their outlet. An area manager gets a consolidated multi-location view with advanced filtering. The owner retains full administrative control - including the ability to grant and revoke access rights without a branch visit or a call to a relationship manager.

Outlet-level data segmentation is non-negotiable. A cashier processing transactions in Mumbai should have zero visibility into Pune’s settlement data. A Maharashtra-level area manager should compare both in a single view - and identify which outlet is underperforming. For a franchise running 30 outlets across two states, this is the baseline operational expectation that aggregators already meet - and the standard every multi-location merchant platform, acquiring banks included, must now match.

A well-designed module should also account for data governance. Every role assignment and access event should be auditable - creating the clean record that responsible merchants require and that RBI’s data governance guidelines expect from platforms handling merchant financial data. [8]

The engagement layer is where the strategic value compounds. StaffAccess is not just an operational tool for merchants - it is an engagement architecture for banks. A cashier who logs in ten times a day to track payments, a store manager who downloads settlement reports every morning, an area manager checking outlet performance across regions - every login is an opportunity.

This is where Mintoak Engage360 becomes relevant. Role-specific nudges can be served to each user tier within the app: a working capital offer to the owner reviewing monthly GMV; a product financing prompt for the manager who just crossed their 500th transaction; a business insurance offer timed to the merchant’s anniversary with the bank. The more the merchant’s team visits the app, the more they see the bank’s financial products - and the more likely they are to take those products from the bank rather than a competitor.

This is where Mintoak SellSmart becomes the natural next layer. It enables banks to surface pre-approved loans, credit cards, and financial products to merchants already active on the platform - with eligibility checks and targeted campaigns that ensure offers reach merchants who qualify, not the entire base. Cross-sell does not begin with a product push. It begins with a platform the merchant's team uses every day.

Area Manager Access: The Retention Feature Banks Are Missing

If a single feature most determines whether a multi-outlet merchant stays or leaves, it is the area manager role - and whether the bank's platform gives that person anything useful to log in for.

A cashier uses the payments app at the point of transaction. A store manager uses it at end of day. But an area manager - overseeing five, ten, or twenty outlets - needs something the typical bank merchant app has never been designed to provide: a consolidated view of how their locations are performing, without calling each store manager individually or waiting for a weekly report.

This is the gap that aggregators have quietly filled. And it is the gap that costs acquiring banks their most valuable merchant relationships.

Mintoak StaffAccess addresses this directly. Acquiring banks can enable merchants to create area manager roles with access to location-wise store performance with advanced filtering across outlets - giving the area manager a single point of visibility into how their region is running. The merchant's operations team stops relying on informal handovers and manual reconciliation. The bank's platform becomes the place where the business is actually managed, not just where payments are settled.

The mobile-first requirement is not incidental. Area managers in Indian retail, food service, and healthcare are field-based, Android-first professionals operating in Tier 2 and Tier 3 cities where connectivity is inconsistent and desk access is limited.

“Tier 2 and Tier 3 markets outperformed metros across nearly every category, signalling deeper smartphone penetration, stronger consumer confidence, and a growing comfort with digital payments outside major cities.” Mintoak Festive Spending Insights 2025 - analysed from 4 million+ SME merchants. [3]

With Tier 3 city merchants leading digital payment value growth at 51% YoY and Tier 2 at 45%, [3] this is the cohort the module must serve - not the metro-based finance manager reviewing a desktop portal once a week. A merchant whose area manager logs in daily to compare outlet performance is not evaluating aggregator alternatives. They are running their business on the bank’s platform. That habitual dependency is worth more than any contractual lock-in.

Implementation Roadmap: From Product Decision to Merchant Adoption

CDOs and product heads evaluate roadmaps by outcomes. Start with three leading indicators that tell you whether the deployment is working:

1. Active non-owner users per merchant account - the signal that role delegation is being used, not just activated.

2. Frequency of area manager logins - the daily login metric that predicts long-term retention.

3. Percentage of role-access merchants deepening their bank product relationship within 12 months - the cross-sell flywheel confirmation.

Phase 1 - Portfolio segmentation. Identify the top 10–15% of the portfolio by GMV and outlet count. These represent the highest churn risk and retention value. Importantly, StaffAccess is available to all merchants regardless of GPV - from a corner salon to a 500-outlet QSR chain. Segmentation identifies where to focus onboarding effort first, not where to limit availability.

Phase 2 - Role architecture validation. Validate role structures directly with merchant operations teams, not through relationship managers. The four-tier model is the starting point, not the ceiling - a pharmacy chain may need a pharmacist role, a QSR chain a shift supervisor tier.

Phase 3 - Build-vs-embed decision. Building natively requires 12 to 18 months of product development, compliance validation, and UAT - during which fintech competitors continue to fill the gap. A pre-built, white-label staff access module can be deployed in weeks: configuration, not construction, with the bank’s brand and credit policies fully preserved - and functioning as a multi-store merchant management platform within the bank’s existing app infrastructure.

Phase 4 - Structured onboarding. Starting with the owner tier, followed by staff role assignment across locations - designed to reduce RM dependency and scale without proportional operational cost. [8] [8]

Beyond StaffAccess: The Full VAS Layer That Makes the Bank App Indispensable

Staff access solves the operational delegation problem. But the strategic ambition is larger: to transform the bank’s merchant app into the operating system for the merchant’s entire business. Mintoak’s VAS suite builds that layer by layer - each module adding a reason for the merchant’s team to open the app daily and find value that no payment aggregator replicates.

-

CustomerInsight - tracks customer lifetime value, visit frequency over 30/60/90-day windows, and enables personalised offers at the point of payment. Converts the payments app into a customer retention tool.

-

DIYOffers - enables merchants to create promotional offers with dynamic segmentation, reward rules, and a performance dashboard. The merchant runs campaigns through the bank’s platform without a third-party tool.

-

MarketingHub - self-service campaign design, custom banners, and tools to drive incremental footfall and attract new customers. Revenue generation, inside the bank-branded app.

-

StoreScore - real-time customer feedback and ratings across outlets, with tools to analyse and improve low-performing locations. Replaces the external survey tool with a native bank capability.

-

AppMarketplace - connects merchants to curated third-party business apps (accounting, inventory, payroll etc) through exclusive bank partnerships, discoverable and manageable within the payments app.

A merchant who uses StaffAccess to delegate operations, CustomerInsight to understand their customer base, and DIYOffers to run promotions is not running their business on a payments app. They are running it on the bank’s platform. The switching cost is measured not in settlement timelines but in operational disruption across their entire team - a switching barrier that no fee waiver replicates.

Frequently Asked Questions

1. What is a staff access module for merchant acquiring banks?

A staff access module enables bank acquirers to give merchants the ability to delegate controlled access to staff - cashiers, store managers, area managers - within the existing merchant payments app. Each role gets configurable permissions over payment acceptance, report downloads, settlement viewing, and outlet-level data, without shared credentials. It converts a single-owner interface into a multi-user business management platform.

2. Why are multi-outlet merchants migrating from banks to payment aggregators?

The migration is driven by an operational sophistication gap, not pricing or settlement speed. Aggregators have built sub-user creation, outlet dashboards, and role-based access as standard. Most bank merchant apps remain single-login interfaces - creating a mismatch with franchise brands, QSR chains, and retail businesses operating five or more outlets. By the time GMV drops are visible to the bank, the settlement account has typically already moved.

3. Does staff access only matter for large, multi-outlet merchants?

No. Even at a single outlet, a business with more than one staff member faces immediate problems: no audit trail, settlement data visible to all, and the owner tied to daily operations. StaffAccess is available to all merchants regardless of GPV or outlet count - from a corner salon to a 500-location QSR chain. It removes the operational constraint that prevents owners from delegating and scaling.

4. Should acquiring banks build staff access natively or use a white-label platform?

Building natively typically requires 12 to 18 months of product development, compliance validation, and UAT - time during which fintech competitors deepen their grip on the merchants anchoring bank portfolios. A pre-built white-label module deploys in weeks, with the bank’s brand, credit policies, and merchant data fully preserved. For most acquiring banks, the speed-to-market advantage of the white-label path is decisive.

5. How does staff access connect to cross-sell and fee income?

Every non-owner user on a role-based merchant app is a daily active user on the bank's platform. Mintoak SellSmart converts that engagement into revenue - surfacing pre-approved loans, credit cards, and working capital offers to merchants via eligibility-based, targeted campaigns. The multi-outlet staff management app builds the daily habit. SellSmart turns it into fee income for the bank.

If your merchant app still serves the owner but not the team running the business, that gap is already costing you. See how Mintoak StaffAccess closes it → contact-us

References

[1] NPCI UPI Monthly Transaction Data, May 2026; ANI / Department of Financial Services, April 2026. UPI: 23.2 billion transactions worth ₹29.9 trillion (May 2026, highest monthly volume on record); 24% YoY growth in transaction count, 19% YoY growth in value (March 2026). P2M payments a growing share of total volume. https://www.npci.org.in/what-we-do/upi/product-overview

[2] Worldline India Digital Payments Report, H1 2025 & RBI Payment Systems Data. UPI QR codes: 7,313 lakh (Dec 2025); POS terminals: 11.2 million (H1 2025). https://worldline.com/content/dam/worldline/local/en-in/documents/main-page11111/Worldline-India-Digital-Payment-Report-1H-2025-1.pdf/

[3] Mintoak Festive Spending Insights, November 2025 (IANS/ET Edge Insights). Analysis of 4 million+ SME merchants on the Mintoak platform. Tier 3 digital payment value: +51% YoY; Tier 2: +45% YoY. https://ianslive.in/emerging-cities-drive-festive-digital-payment-value-at-smes-by-44-pc--20251120115734

[4] The Economic Times, “PSU Banks Counting on QR-Based Payments to Breach a Fintech Fort,” January 22, 2026. https://economictimes.indiatimes.com/tech/technology/psu-banks-counting-on-qr-based-payments-to-breach-a-fintech-fort/articleshow/127036324.cms

[5] The Economic Times, “Banks to Take on Fintechs with Feature-Packed Merchant Apps,” 2024.

[6] Raman Khanduja, CEO, Mintoak - quoted in The Economic Times, January 22, 2026 (see reference [4]).

[7] PwC India, “Payment Aggregators and Payment Gateways,” 2023. https://www.pwc.in/assets/pdfs/consulting/financial-services/fintech/publications/payment-aggregators-and-payment-gateways.pdf

[8] Reserve Bank of India, Master Direction on Payment Aggregators, September 15, 2025. RBI/2025-26. https://www.rbi.org.in/

[9] NPCI, UPI Product Overview and Merchant API Interoperability Guidelines. https://www.npci.org.in/what-we-do/upi/product-overview

[10] PIB / Ministry of Finance - UPI QR Merchant Deployment Data: 56.86 crore QR codes deployed to ~6.5 crore merchants, FY 2024–25. https://www.pib.gov.in/PressReleasePage.aspx?PRID=2200569

Conclusion

The retention opportunity is not in competing on pricing or settlement timelines. Aggregators hold structural advantages in both. The opportunity is in a different category: becoming the operational infrastructure that merchant teams depend on daily.

A role-based merchant app - banks that build this capability and pair it with area manager dashboards within the next 12 to 18 months - will create switching barriers far more durable than any loyalty incentive or fee waiver. Not because merchants are locked in - but because their cashiers, store managers, and area managers are running their business on the bank’s platform every day.

The Merchant Retention Blueprint is a product strategy, not a relationship strategy. It requires building features that serve the merchant’s entire team - not just the account owner - and layering VAS capabilities that give every user a reason to open the app beyond payment acceptance.

Every merchant that grows past five outlets is a test the bank either passes or fails silently. Pass it with the right platform and the relationship deepens. Fail it, and the settlement account moves before the relationship manager knows there was a problem. The window to act is open. The merchants scaling right now will not wait.

Mintoak StaffAccess gives bank acquirers a proven, deployable path to get there. Talk to Mintoak → mintoak.com/contact-us

Share on your socials

Copy Link

Checkout other blogs