Generated by AI

From Transaction to Engagement: Building a Merchant Cross-Sell Engine for Merchant Acquirers

7 mins

●

ByMintoak

●

10 Jun 2026

Copy Link

The Acquirer's Dilemma: Revenue Compression Meets Relationship Opportunity

There is a quiet crisis playing out across India's acquiring bank portfolios - and most banks are still treating it as a payments problem.

MDR compression, the UPI zero-MDR mandate, and competition from fintech aggregators have steadily eroded the economics of merchant acquiring. Revenue per terminal has declined. The service cost each merchant has not. And yet, the merchant base inside every acquiring bank's portfolio is arguably one of the most undervalued financial assets in Indian banking today.

Banks process crores of rupees in merchant transactions every month - accumulating behavioural and financial intelligence that no credit bureau, no NBFC, and no fintech competitor can replicate from the outside. Yet the relationship almost exclusively stays at the transactional layer. Settlement in, settlement out, repeat.

The merchant's working capital need, insurance gap, or business financing requirement goes unaddressed – and is eventually filled by a competitor. The data suggests it doesn't have to be. Banks that have deployed a structured merchant engagement layer have seen 55% of active merchants engage with cross-sell products and a 4.5x lift in app-driven cross-sell. [6]

Why Merchant Acquirers Are Sitting on an Untapped Revenue Goldmine

The scale of the opportunity is not theoretical. India's MSME sector has crossed 7.94 crore Udyam registrations as of May 2026. [1] Yet only 18% of Indian MSMEs have accessed digital lending, [2] meaning the vast majority of merchants being served by acquiring banks have never received a financial product from the very bank processing their payments. Every acquiring bank processing merchant payments is sitting on a level of transactional intelligence that no credit bureau, no NBFC, and no external fintech can replicate – the equivalent of months of financial due diligence, generated automatically with every settlement.

It knows which merchants are growing, which are seasonal, which are consistent, and which are stressed - before any credit bureau does. PSU banks have recognised this. SBI, Punjab National Bank, and Central Bank of India are now committing resources to QR-code-led merchant acquisition, moving into territory long dominated by BharatPe, PhonePe, and Paytm. [3] The numbers signal the prize.

RBI data shows 728 million QR codes deployed across the country versus just 11 million POS terminals. [4] NPCI data shows ₹8 lakh crore moved through 13 billion UPI merchant transactions in December 2025 alone - 67% of those transactions were above ₹2,000. [3]

Raman Khanduja, CEO of Mintoak, articulated exactly why the payment layer is the starting point, not the end point: "Banks are focusing on making their payment platforms more relevant through features like instant onboarding and on-demand settlement. With an existing strong banking relationship, once the payment layer is solid, adding credit and related products becomes much easier."

The shift from payment processor to merchant financial partner is not just a product decision. It directly impacts fee income, CASA growth, and long-term merchant book quality.

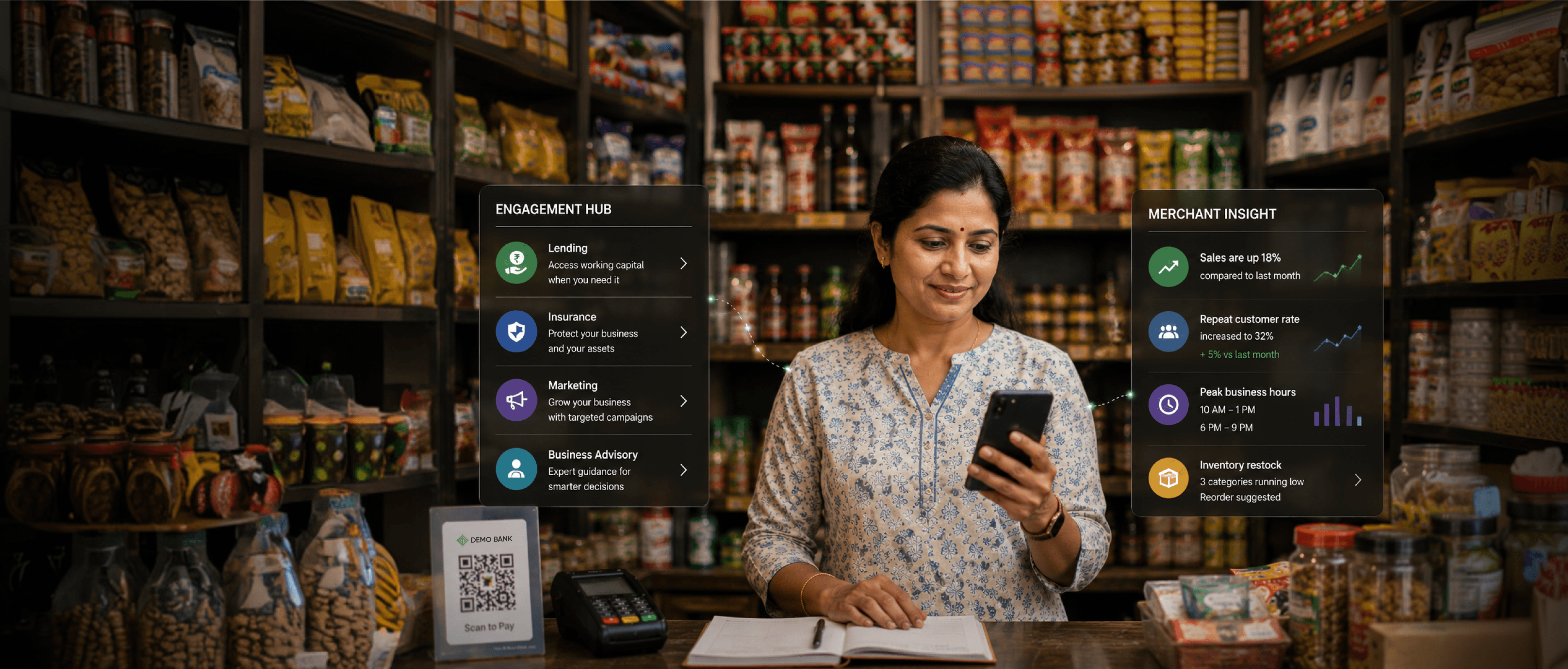

The Architecture of a Merchant Cross-Sell Platform

A merchant cross-sell engine is a platform with 3 integrated layers.

-

The data layer ingests real-time transaction streams from POS, QR, UPI, and card rails; merchant profile data including KYC and GST filings; and behavioural signals like settlement patterns, dispute rates, and category trends. Together, these feed a continuously updated merchant propensity score - a live read on which merchant is ready for which product, right now.

-

The decisioning engine combines rule-based triggers with ML propensity models. A merchant whose monthly GMV crosses ₹10 lakh for three consecutive months automatically enters a pre-approved working capital offer queue. A merchant with a clean settlement history becomes eligible for a credit card or overdraft offer - without a relationship manager manually reviewing every case.

-

The product orchestration layer connects the decisioning engine to core banking systems, NBFC co-lending APIs, insurance aggregators, and the merchant-facing payments app - where the offer surfaces not as a cold interruption, but as a contextually relevant nudge while the merchant reviews their settlements. The core insight here: cross-sell doesn't happen because a product is available. It happens because a merchant is engaged. Build the engagement layer first. Cross-sell follows.

Merchant Creditworthiness: Moving Beyond CIBIL

India's formal credit infrastructure systematically excludes the majority of merchants - particularly Tier 2/3 merchants, informal retailers, and first-generation business owners.

Acquiring banks already hold the alternative data that resolves this.

Transaction velocity, ticket size stability, settlement inflow consistency, chargeback ratios, and GST filing regularity together form a Merchant Financial Health Score that is often more predictive of repayment behaviour than a CIBIL score alone.

Seasonality matters too. A textile merchant whose GMV spikes 3x during Navratri isn't experiencing volatility - they're demonstrating a predictable revenue pattern. That's a pre-Diwali working capital offer waiting to happen, with repayment timed to their settlement cycle. The gap isn't data. It's the platform and decisioning layer to convert that data into a structured offer.

Key Products Across the Merchant Lifecycle

The merchant lifecycle demands a differentiated product stack - not a one-size-fits-all offer.

Newly onboarded merchants need QR/POS hardware financing, Soundbox subscriptions, and basic business insurance.

Growing merchants - those with consistent GMV growth - are prime candidates for merchant cash advances, working capital overdrafts, business credit cards, and health and life insurance.

Mature merchants benefit from virtual credit cards, fixed deposits, payroll management, and staff access controls - building the kind of operational stickiness that makes switching banks genuinely costly.

The fulfilment design that works: offer surfaces in the merchant payments app, disbursal goes directly into the settlement account, repayment is auto-debited from future settlements. No collateral. No branch visit. No friction.

White-Label vs. Build In-House

Building in-house offers control - but typically requires 18 to 36 months and significant investment in ML, regulatory tech, and API engineering. Most acquiring banks cannot afford that timeline, while fintech competitors fill the gap.

White-label platforms purpose-built for bank acquirers can be deployed in 8 to 16 weeks - with the bank's brand, credit policies, and merchant data fully preserved. No ground sales team needed for cross-sell. Targeting, communication, and lead capture happen digitally.

Mintoak's SellSmart is built for exactly this: cross-selling pre-approved loans, credit cards, and financial products through the merchant payments app; assessing creditworthiness from transaction data; integrating APIs for eligibility checks and lead capture - without the acquirer building any of it from scratch.

IRCTC's fintech move illustrates the broader principle. When IRCTC received its payment aggregator licence from RBI in August 2025, the conversation immediately moved beyond payments to what the underlying data could unlock.

As Raman Khanduja observed: "IRCTC is sitting on a goldmine of data. To cross-sell services, you need data. And nothing generates nuanced data like payments." [5]

And on the revenue potential: "As a full-service payment aggregator, IRCTC could extend beyond ticketing to credit, insurance, loans and more - building 4 to 5 new revenue lines for the same customer." [5]

The analogy for acquiring banks is exact. The payments app is the engagement layer. Mintoak SellSmart converts that engagement into measurable product revenue.

The ROI Case

The numbers from live deployments make the case clearly.

Mintoak's data shows 55% of active merchants engage with cross-sell products when those products are embedded in the payments app and surfaced through targeted campaigns. App-driven cross-sell increases 4.5x with a structured engagement layer - dynamic segmentation, omnichannel campaigns, AI-personalised content.

These are not cold outreach conversion rates. They are the result of reaching pre-qualified merchants, in context, through a merchant payments app they already use daily, which offers solutions beyond payment acceptance.

The cost comparison is equally sharp. A ground sales team calling on merchants carries a cost-per-lead that scales linearly - travel, time, rejection rates. A digital cross-sell platform deploys campaigns to pre-qualified segments at marginal cost that doesn't grow with the portfolio.

The four metrics that matter for the internal business case:

- Cross-sell conversion rate on targeted campaigns.

- Cost per acquired product versus field-based acquisition.

- Merchant retention improvement for product-holding merchants.

- Incremental fee income per merchant per year.

Together, these metrics tell a compounding story – each product a merchant holds deepens the relationship, reduces churn risk, and increases the revenue contribution of that merchant to the bank's portfolio over time.

Frequently Asked Questions

1. What is a merchant cross-sell platform for bank acquirers?

A merchant cross-sell platform enables bank acquirers to offer financial products - loans, insurance, credit cards - directly to merchants through their payments app. It uses transaction data to assess creditworthiness, identify eligible merchants, and deliver targeted offers digitally. Instead of relying on ground sales teams, banks can run automated, personalised campaigns that convert payment relationships into full financial partnerships at scale.

2. How can banks use merchant transaction data for cross-selling?

Every payment a merchant processes reveals behavioural and financial signals - GMV trends, settlement consistency, seasonal patterns, ticket size stability. Banks can use this data to build a Merchant Financial Health Score that predicts credit eligibility more accurately than traditional bureau scores. This enables pre-approved loan offers, insurance products, and other financial services to be surfaced at the right moment, to the right merchant.

3. What financial products can bank acquirers cross-sell to merchants?

Bank acquirers can cross-sell working capital loans, merchant cash advances, overdraft facilities, business credit cards, virtual credit cards, life and health insurance and fixed deposits. The right product depends on the merchant's lifecycle stage - newly onboarded merchants need different products than high-GMV merchants with established transaction histories. A structured cross-sell platform matches product to merchant automatically.

4. Should banks build a merchant cross-sell engine in-house or use a white-label platform?

Building in-house typically takes 18 to 36 months and requires significant investment in machine learning, compliance infrastructure, and API integrations. A white-label merchant cross-sell platform purpose-built for bank acquirers can be deployed in 8 to 16 weeks, with the bank's brand and credit policies fully preserved. For most acquiring banks, the speed-to-market advantage of a white-label solution outweighs the control benefits of an in-house build.

5. What ROI can bank acquirers expect from a digital merchant cross-sell solution?

Mintoak's deployment data shows 55% of active merchants engage with cross-sell products when offers are embedded in the payments app through targeted campaigns - with a 4.5x increase in app-driven cross-sell. Beyond conversion rates, the ROI framework covers cost per acquired product versus field-based acquisition, merchant retention improvement, and incremental fee income per merchant annually - all metrics that compound as the merchant portfolio scales.

References

[1] MSME Ministry, Udyam Registration Portal, May 2026. https://udyamregistration.gov.in/

[2] SIDBI, "Understanding Indian MSME Sector" Report, May 2025. https://www.sidbi.in/

[3]The Economic Times, January 22, 2026 - PSU banks counting on QR-based payments to breach a fintech fort. Raman Khanduja, CEO Mintoak, quoted in same article https://economictimes.indiatimes.com/tech/technology/psu-banks-counting-on-qr-based-payments-to-breach-a-fintech-fort/articleshow/127036324.cms

[4]Reserve Bank of India, "Reserve Bank of India (Digital Lending) Directions, 2025," RBI/2025-26/36, May 8, 2025. https://www.rbi.org.in/

[5]The CapTable, August 2025, IRCTC boards the fintech express, eyeing a bigger retail and e-commerce play. https://the-captable.com/2025/08/beyond-railway-irctc-payment-licence-fintech-ecommerce-play/

[6]Mintoak Engage360 - ‘Merchant Lifecycle Management Platform, Impact Data’. https://www.mintoak.com/products/mintoak-engage360

Additional: NPCI UPI Product Statistics · IFC MSME Finance Gap 2025 · GSTN · Sahamati Account Aggregator · BIS Working Paper 1062

Conclusion: From Payment Rail to Relationship Bank

Merchant acquiring portfolios are not payment infrastructure assets. They are relationship assets – pre-qualified, behaviour-rich, financially underserved cohorts waiting for the bank to show up as a financial partner rather than a settlement machine.

The technology exists. The regulatory infrastructure is mature. Merchant digital readiness in India has never been higher. What has been missing is the framing.

Cross-sell is not a product bolted onto a payments platform. It is an engagement strategy where the merchant payments app becomes the surface through which a bank progressively deepens its financial relationship with every merchant in its portfolio. Done right, a merchant cross-sell engine doesn't just add revenue lines. It redefines what the acquiring relationship means. The merchants are already on the app. The transaction data is already there. The competitive window - before fintechs and neo-banks fill the void - is open, but not indefinitely.

Mintoak's SellSmart gives bank acquirers a proven, deployable path to get there - without the 18-month build, without the ground sales team, and without leaving merchant financial needs unaddressed. Talk to us at mintoak.com.

Share on your socials

Copy Link

Checkout other blogs